Bank of America is one bank that is not one of the sharpest knives in the drawer when it comes to hiring the best employees. This takes the cake…

I was on a business trip in Barcelona, Spain, for a week, so I was a bit behind on errands and other life stuff.

Like checking my mail.

On Sunday, I finally caught up and checked my mail for the first time in about six days.

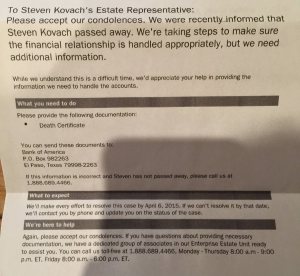

The first letter I opened was this one from Bank of America, where I have checking and savings accounts:

The second letter I opened was another one from Bank of America apologizing for the first letter and assuring me I’m still alive.

Source: Business Insider