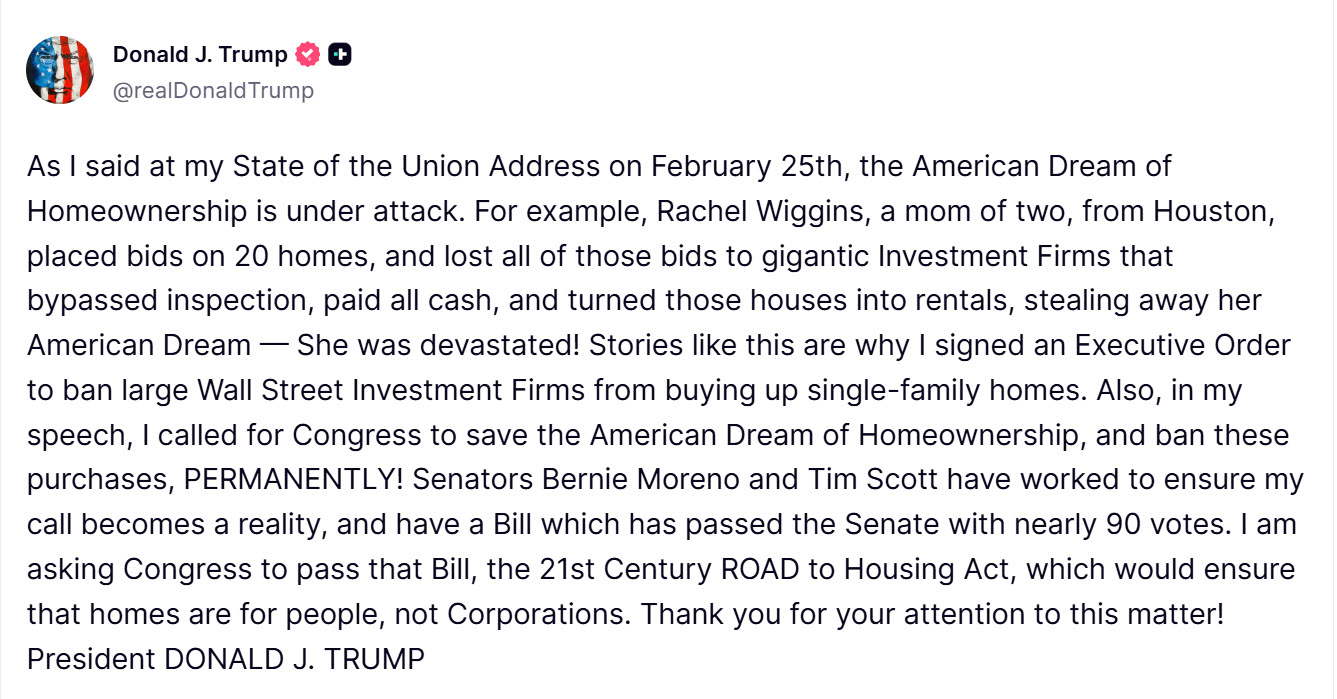

And has been for several decades. A Truth Social post 5/11/2026:

Nov. 14, 2025 — With all this new talk about mortgage fraud and funding or selling Fannie and Freddie, it may be time to revisit where the mortgage fraud and fraudulent financial products started.

The recent lawsuits filed in the SUPREME COURT OF THE STATE OF NEW YORK, COUNTY OF NEW YORK are the beginning of a long process unraveling the frauds created by a generation of “Younger Boomers” and “Now Generation” Wall Street bankster executives that expected immediate gratification.

The recent lawsuits filed in the SUPREME COURT OF THE STATE OF NEW YORK, COUNTY OF NEW YORK are the beginning of a long process unraveling the frauds created by a generation of “Younger Boomers” and “Now Generation” Wall Street bankster executives that expected immediate gratification.

These smart-asses didn’t take the time to ensure all the pieces to the puzzle fit before they began their filthy rich land grab operation, causing a lot of damage and red ink to America and the rest of the world. Their failures are your insurance to defeat foreclosure once you understand what is missing. Continue reading

By Sydney Sullivan

For a direct link to the video click on the picture above.

“Through this Act, the People call upon their government to act decisively: to audit and recover all stolen property and records, to dismantle corrupted networks, and to ensure that such crimes can never again be hidden behind technology or private monopolies. This Act is the lawful bridge between historic duty and modern enforcement — uniting the past, present, and future of our Republic in a single demand for justice and restoration.” H.R. 1776 Please read and Share.

Continue readingBy Shelley Erickson

Foreclosures are traumatic. Many have become life-threatening, deadly weapons, creating disease, suicide, heart attacks and numerous other illnesses that have stemmed from fraudulent financial products issued by the banks and some with oversight by Fannie Mae.

But not all Courts of Appeal have agreed with that Saterbak approach.

In Brown v. Deutsche Bank National Trust Co., the court acknowledged some decisions — like Saterbak — holding that borrowers cannot bring “preemptive” attacks on the assignment of a deed of trust before a foreclosure sale. But, the court observed, the reasoning in Yvanova “raises the distinct possibility that our state Supreme Court would conclude that borrowers have a sufficient injury, even if less severe, to confer standing to bring similar allegations before the sale.”

Ultimately, the court held that it did not need to decide that issue, because the appeal could be resolved on other grounds.

The Brown opinion was covered on Money and Dirt here: The Simplest Way to Defeat Claims Alleging an Invalid Assignment of a Deed of Trust: Judicially Noticeable Documents.

Advertisement

https://www.gofundme.com/f/please-help-our-homeless-cat-community

This about sums it up perfectly. Nobody knows better the corruption in the court rooms than the American Homeowners.

For 17 years American Homeowners have fought the banksters and their fraudulent UNREGULATED DERIVATIVES securitization scam – some successfully, some not.

BOTTOM-LINE – We’re tired of the fabricated documents, cleverly worded, but still false declarations, failure to prove standing – and especially using significantly reduced photocopies of an alleged Promissory Note, undated allonges and/or unsigned endorsements left “in blank” to further their fraud. Along with fraudulent Assignments of Mortgage, created or ordered by questionable law firms for the banks and many times back-dated, if dated at all. And let’s not forget the lower court foreclosure judges that let the Plaintiff Bank get away with it!

Continue reading“The moral hazard lies with the banksters’ and their cohorts’ deception and intent to deceive, the failure to disclose, the intentionally inflated appraisals and the sick and intentional manipulation of the American homeowners’ reliance for the one and only purpose of demented capitalistic profit. When you make a photo copy of a negotiable instrument or cash and try to pass it off as an original – there is intent to deceive.”

“The saddest outcome of all of this is that the judges and the governments think they are holding the country together, when in fact, by allowing this type of man-made computerized criminal behavior they are merely adding to the country’s overall moral degradation and physical decay. And for what? For pensions, retirement funds and investments that, more than likely, are not there anymore anyway? Wake up!”

There’s no difference in photocopy reductions of a Mortgage Note passed off as an ORIGINAL Note, than the counterfeiting criminal trying to copy and print currency. Nor is there a difference between a Judge accepting an obvious reduced photocopied Note instead of a wet ink ORIGINAL, than the criminal getaway driver who is an accessory to the crime. IMHO.

This is one series you don’t want to miss. The banks are coming back at the homeowners even when they were originally DISMISSED WITH PREJUDICE. We always knew they had unclean hands and dirty paper – now they are proving the homeowners right!

By Sydney Sullivan

How to Prove Innocence When Falsely Accused of

johnny brown, attorney

Sexual Assault – Part 3

“…and if we were able to settle the civil case for $150,000.00 that she would leave the island and not appear at the trial of the criminal case.”

Aloha, and may God inspire you to follow this story.

Just wait until the Circuit Court finds out the Text Exhibits used at trial

were manipulated!

This was the first post on GoFundMe, that lasted less than a day. GoFundMe took it down without warning and said at first it was due to policy issues. It took 3-5 days to return the monies to the donors. The 2nd post Doc created was so simple and brief it couldn’t conflict with policy issues. But once donors hit $10K level – GoFundMe again took it down and this time admitted that someone complained. Someone desperate enough to suppress the truth. And when you continue to read the details of this sorted story –

you’ll begin to understand why.

When one opts to study medicine, they are opting for a career that is unlike any other, it is a calling. The job is to help reduce suffering. The first oath taken upon entering the profession is: “A physician shall uphold the dignity and honour of his profession.” And the first declaration made is “I solemnly pledge myself to consecrate my life to service of humanity.” Doctors are professionals and most are not businessmen. Their first thought is about helping others without judgment, so it’s understandable how any doctor could become an easy mark.

Dr. Curtis Bekkum has been caring for the Hana, Lahaina, and Central Maui, Hawaii communities open-heartedly since the day he began practicing medicine in Hawaii. The communities know that health care is never refused in his offices, and it has never been about money. Care always comes first.

We need to reach out to everyone for support as Dr. Bekkum is going through an unjust legal battle that requires substantial funds to prove his innocence. Not all allegations of any crime, including sexual assault, are real. Please DONATE, no matter the amount to Venmo@Curtis-Bekkum. Once again, there has been an alternative donation site established. Click HERE to donate.

Continue reading