When all is said and done the courts come back to the main premise, “Did you pay?”. That is so injudicious on so many levels. The deeper we get into securitization and contract law we soon realize (after dissection) there is one very basic question being ignored – “Is the Promissory Note even enforceable?”

When all is said and done the courts come back to the main premise, “Did you pay?”. That is so injudicious on so many levels. The deeper we get into securitization and contract law we soon realize (after dissection) there is one very basic question being ignored – “Is the Promissory Note even enforceable?”

Sheila Bair’s (former FDIC Chairperson) new book, Bull By the Horns, addresses issues that must be taken into careful consideration when considering the validity of foreclosures – and she does it with impressive candor. Sheila separates the MBS into 2 categories: NTMs (nontraditional mortgages) and subprime loans. Apparently, they are not one in the same. However, this is where disputes of validity actually begin. NTMs – were not traditional mortgages but no one disclosed that to the homeowners.

The promissory notes in these NTMs and subprime loans are like the Titanic. By its very make-up it appears the promissory note enforce-ability is sinking out of control. It appears the loans were never properly assigned to the trusts, but that’s not the only problem.

To understand the promissory note issues you need to review certain regulatory events and comprehend contract law and how it applies in this new realm of NTMs and subprime loans. These nontraditional mortgages (after the turn of the century) were a new breed of securitization. The lending practices that Ms. Bair and her staff had viewed as “predatory” in 2001 had become “mainstream among most major mortgage lenders” by 2006. By repealing Glass-Steagall in 1999 (thanks to President Clinton and the 1990’s Republican Congress), the door had swung wide open allowing the banks to run amok with very little regulation (if any) and questionable oversight (if any at all).

To understand the promissory note issues you need to review certain regulatory events and comprehend contract law and how it applies in this new realm of NTMs and subprime loans. These nontraditional mortgages (after the turn of the century) were a new breed of securitization. The lending practices that Ms. Bair and her staff had viewed as “predatory” in 2001 had become “mainstream among most major mortgage lenders” by 2006. By repealing Glass-Steagall in 1999 (thanks to President Clinton and the 1990’s Republican Congress), the door had swung wide open allowing the banks to run amok with very little regulation (if any) and questionable oversight (if any at all).

In addition to the repeal of a law in 1999 that had protected homeowners since 1933, Congress also passed the ELECTRONIC SIGNATURES IN GLOBAL AND NATIONAL COMMERCE ACT (E-Sign) in 2000. “What?”, you say?? What does that have to do with mortgages and promissory notes?

Devious planning by the banks had schmoozed legislators into passing a law allowing your signature on any document (with very few exceptions) to be transferred electronically – if you gave your explicit agreement and authorization. That was the consumer protection “safe harbor” provision that made it into both (E-Sign and UETA). E-Sign is the federal version of the state ratified Uniform Electronic Transactions Act (UETA). How many homeowners were aware of E-Sign and UETA when they signed their mortgage loans? Raise your hands? Did your loan officer disclose to you that your explicit agreement to electronic transfers of the loan was necessary? Nah – didn’t think so. It was a well kept secret because as most people comment when asked this question, “hell no!”

The hard core fact here is that in order to securitize the loan documents – they need to be electronically transferable. Step one – not done.

The hard core fact here is that in order to securitize the loan documents – they need to be electronically transferable. Step one – not done.

While failure to get explicit agreement from the homeowner for electronic transfers does not nullify the underlying contracts – it does leave the door open to question the contracts under state law.

See Electronic Records and Signatures under the Federal E-SIGN Legislation and the UETA

fn. 67. While not affecting the continued validity of the contract, “[f]ailure to obtain electronic consent or confirmation of consent would . . . prevent a company from relying on section 101(a) to validate an electronic record that was required to be provided or made available to the consumer in writing.” 146 CONG. REC. S5220 (daily ed. June 15, 2000) (statement of Sen. Leahy).

There is also very interesting paper written in 1999 by R. David Whitaker called:

Rules Under the Uniform Electronic Transactions Act for an Electronic Equivalent to a Negotiable Promissory Note

Mr. Whitaker was the Reporter for the Standards and Procedures for electronic Records and Signatures (“SPeRS”). He also served as Reporter for the Mortgage Bankers Association white paper “Security Interests in Transferable Records.” He was an active participant in the drafting of Revised Articles 5 and 9 of the UCC. He participated in the drafting of the Uniform Electronic Transactions Act, where he chaired the Task Force on Scope and served as reporter for the Task Force.

Mr. Whitaker was the Reporter for the Standards and Procedures for electronic Records and Signatures (“SPeRS”). He also served as Reporter for the Mortgage Bankers Association white paper “Security Interests in Transferable Records.” He was an active participant in the drafting of Revised Articles 5 and 9 of the UCC. He participated in the drafting of the Uniform Electronic Transactions Act, where he chaired the Task Force on Scope and served as reporter for the Task Force.

Mr. Whitaker also advised industry participants on the creation and drafting of the federal Electronic Signatures in Global and National Commerce Act. He is one of the co-authors of The Law of Electronic Signatures (West).

If you are a warrior (and some aren’t) or if you are a negotiator you should probably click on the title link above and read this paper. You really need to read the whole paper but here are some important segments (click on the clip below to increase and read):

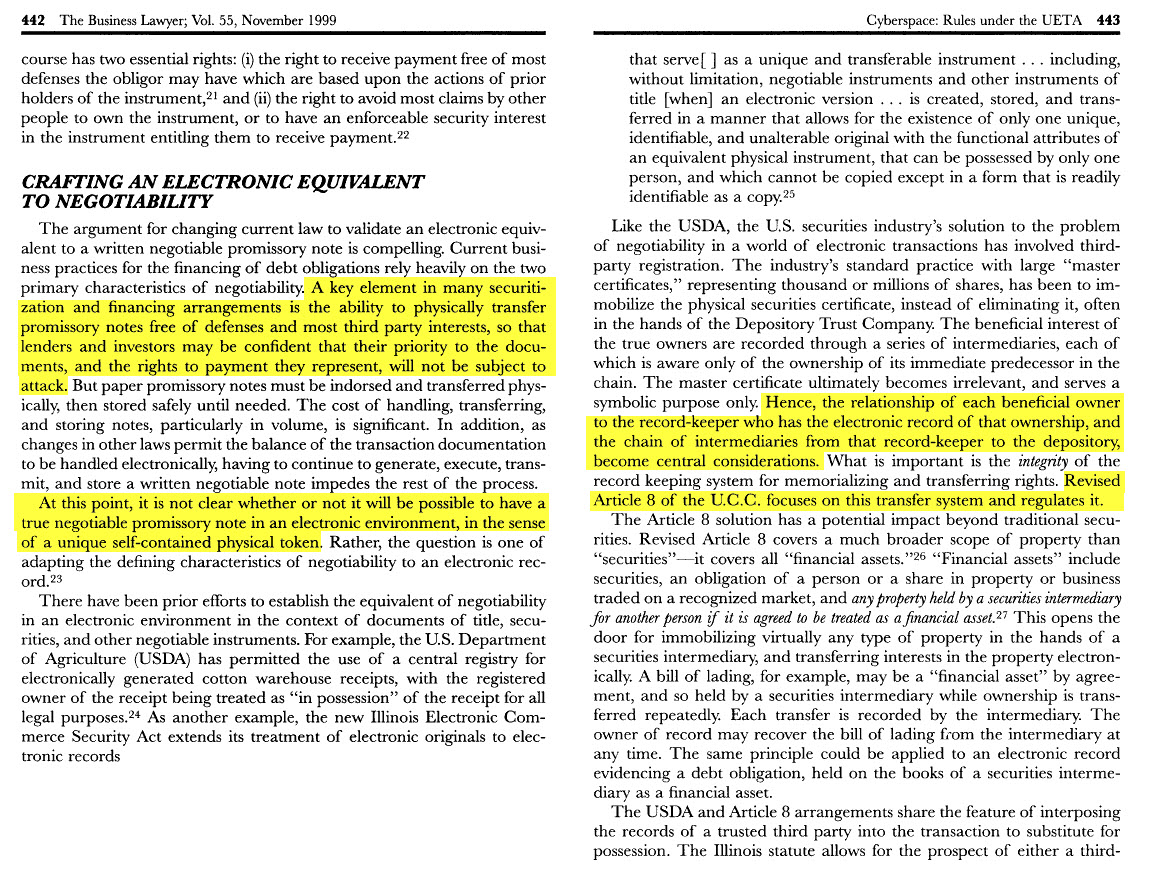

Even in 1999 the creators and advisers of these electronic signature acts weren’t at all certain just how well they would fly. Whitaker writes, “[A]t this point, it is not clear whether or not it will be possible to have a true negotiable promissory note in an electronic environment, in the sense of a unique self-contained physical token.” Here we have homeowners thinking they are contracting for a traditional mortgage when in fact behind the scenes it has already been designated as a securities instrument. Voila! You sign a negotiable instrument that is “intended” to be whisked away and materially altered into a securities certificate under UCC Article 8 – but you don’t know it. It was not disclosed to you. Step two – no do.

It certainly appears these promissory notes were designed to be transferred and reckoned with under UCC Article 8 – not Article 3. Article 8 governs a broader scope than just “securities” – it covers all “financial assets” including securities “and any property held by a securities intermediary for another person if it is agreed to be treated as a financial asset,” writes Whitaker. He ends with the point that the obligor (borrower) is entitled to have access to the authoritative copy. And it appears courts in the past have felt that only the originals can provide sufficient warranty and clarification.

For nearly 14 years the banking industry has been stumbling, fumbling and fouling the homeowners and the American public in an un-perfected process that is full of holes. The courts are trying to navigate… but it’s like playing football in a swamp during a tsunami. Most attorneys slept during Uniform Commercial Code lectures (karma is a bear) and so now we are faced with challenging the validity and enforce-ability of contracts where there were no disclosures, no meeting of the minds and a future intent that had already taken place – but with no detail or disclosure to the homeowner. Don’t think for a minute that securitization didn’t take its toll which will be haunting the housing market for years.

For nearly 14 years the banking industry has been stumbling, fumbling and fouling the homeowners and the American public in an un-perfected process that is full of holes. The courts are trying to navigate… but it’s like playing football in a swamp during a tsunami. Most attorneys slept during Uniform Commercial Code lectures (karma is a bear) and so now we are faced with challenging the validity and enforce-ability of contracts where there were no disclosures, no meeting of the minds and a future intent that had already taken place – but with no detail or disclosure to the homeowner. Don’t think for a minute that securitization didn’t take its toll which will be haunting the housing market for years.

Another interesting document is Contracts 2.0: Making and Enforcing Contracts Online. Online contracts also have the UETA and E-Sign necessity. While many homeowners used Internet or phone and email in their loan process – it still requires notification, explicit agreement and clearly a “meeting of the minds”.

- A “meeting of the minds” must exist with respect to each material issue in the agreement. Montagna, 269 S.E.2d at 845; Scott v. Pacific Gas & Elec. Co., 904 P.2d 834, 841 (Cal. 1995).

- Failure to agree on essential terms of a contract indicates a lack of mutual assent. Id.

- Online agreements must demonstrate both parties intend to be bound.

See Feldman v. Google, Inc., 513 F. Supp. 2d 229, 236

(E.D. Pa. 2007). See generally Martin v. Snapple Bev.

Corp., No. B174847, 2005 Cal. App. Unpub. LEXIS

5938, at *15 (Cal. Ct. App. July 7, 2005) (Whereas

browse-wrap license agreements are part of the website

and the user assents to the contract when the user visits

the website, a click-wrap license/agreement permits the

consumer to manifest his or her consent to the terms of a

contract by clicking on an acceptance button.”).

![]() While online agreements cover a good deal of Internet activity; promissory notes, however, are viewed a bit differently. Even if it was downloaded from the Internet – UETA still mandates that the explicit agreement be made at the time of issuance…

While online agreements cover a good deal of Internet activity; promissory notes, however, are viewed a bit differently. Even if it was downloaded from the Internet – UETA still mandates that the explicit agreement be made at the time of issuance…

Check your mortgage and note – do you see any explicit notations relating to UETA “safe harbor” clauses that you signed?

-

- Mutual assent is determined under an objective standard: what would a reasonable person think of the meaning of the outward expressions of the parties? See Costar Realty Information, 612 F. Supp. 2d 660, 669 (D. Md. 2009); Cochran v. Norkunas, 919 A.2d 700, 710 (Md. 2007)

■ Definitiveness of Terms.

- Terms of the agreement should be clear and unambiguous, and it is the duty of a court, not a jury, to determine if a valid contract exists. See W.J. Schafer Assocs., Inc. v. Cordant, Inc.., 493 S.E.2d 512, 519 (Va. 1997).

- When plain and unambiguous, a court must presume parties meant what they expressed, and will not consider what parties may have subjectively intended. See Cochran, 919 A.2d at 710.

- Ambiguity arises if a reasonable person would believe language is susceptible to more than one meaning.

- A contract must be construed in its entirety. Id.; City of Los Angeles v. Superior Court of the County of Los Angeles, 333 P.2d 745, 750 (Cal. 1959).

All of these issues affect the overall validity of a contract – and it appears are rarely plead before the foreclosure courts by competent attorneys. As noted earlier – there are warriors and there are negotiators… and it all depends upon how much your judge or the appellate court will comprehend and how well it is argued.

All of these issues affect the overall validity of a contract – and it appears are rarely plead before the foreclosure courts by competent attorneys. As noted earlier – there are warriors and there are negotiators… and it all depends upon how much your judge or the appellate court will comprehend and how well it is argued.

One of the more essential elements that addresses the lack of disclosure about securitization falls under:

Agreement to Agree

See City of Los Angeles v. Superior Court of the County of Los Angeles, 333 P.2d 745, 750 (1959); see also W.J. Schafer Assocs., Inc. v. Cordant, Inc., 493 S.E.2d 512, 519 (Va. 1997) (arguing contract was agreement to agree and thus too vague and indefinite to enforce).

- A promise to agree in the future is not binding on the parties, and therefore creates a failure of consideration.

Rule: If essential element of a promise is reserved for future agreement, the promise gives no rise to legal obligations until the future promise is made. See City of Los Angeles, 333 P.2d at 750

- Depends on relative importance and severability of future matter. Id.

- If unessential, parties must accept reasonable determination of unsettled point. Id.

Let’s take a look at that “may transfer” clause in the Promissory Note. The originator or lender “may transfer” the note. It does not say the lender “will” transfer the note, or “is going to” transfer the note, or even “already has transferred the note. The clause quite clearly infers that “sometime in the future” the lender “may” transfer the note to someone else. “May” as defined by a law dictionary (8th ed. 2004) is futuristic:

may, vb. 1. To be permitted to <the plaintiff may close>. [Cases: Statutes 227. C.J.S. Statutes §§ 362–369.] 2. To be a possibility <we may win on appeal>.

Transfer, is also well defined:

transfer, n.1. Any mode of disposing of or parting with an asset or an interest in an asset, including a gift, the payment of money, release, lease, or creation of a lien or other encumbrance. • The term embraces every method — direct or indirect, absolute or conditional, voluntary or involuntary — of disposing of or parting with property or with an interest in property, including retention of title as a security interest and foreclosure of the debtor’s equity of redemption. 2. Negotiation of an instrument according to the forms of law. • The four methods of transfer are by indorsement, by delivery, by assignment, and by operation of law. [Cases: Municipal Corporations 917. C.J.S. Municipal Corporations §§ 1658–1660.] 3. A conveyance of property or title from one person to another. [Cases: Bills and Notes 176–222. C.J.S. Bills and Notes; Letters of Credit§§ 4, 29, 139–141, 143–159.]

“May transfer” when dissected appears to mean “sometime in the future” the lender might dispose of its interest in this note to someone else. The kicker is that in securitization (in most cases) the warehouse lender / investment bank had already taken the “transfer” when it funded the loan before the homeowner ever signed. It did not happen in the future – it had already occurred and there was no disclosure, meeting or the minds or mutual assent.

“May transfer” when dissected appears to mean “sometime in the future” the lender might dispose of its interest in this note to someone else. The kicker is that in securitization (in most cases) the warehouse lender / investment bank had already taken the “transfer” when it funded the loan before the homeowner ever signed. It did not happen in the future – it had already occurred and there was no disclosure, meeting or the minds or mutual assent.

What if we go back to contract law and drive the point home that there was securitization already in play, that the originator failed to obtain explicit agreement to electronically transfer the documents per UETA, that the mortgage was intentionally designed to skirt the consumer safe harbor of UETA, and that the clause in the note the “lender may transfer the note” (in the future) wasn’t clearly defined; when in fact it had already been pledged and paid for in a securitization transfer; and, undisclosed to the homeowner – would it not be “far too central” to the transaction when it appears “there was never any intention to enter into a binding contract” by the originator?

Would not an essential aspect of this NTM (nontraditional mortgage) be the securitization intention of this loan – and it had not been disclosed or completely determined? And due to the securitization and the material alteration of the negotiable instrument under UCC Article 3 morphing into a mortgage-backed securities under UCC Articles 8 & 9 without disclosure – doesn’t that seem like a pretty central issue to the contract – no matter when it happened?

CABLE COMPUTER TECHNOLOGY INC v. LOCKHEED SANDERS INC

As the court opined: “The majority might respond that there is no need to decide those questions; the only issue is whether the parties bargained in good faith-that is, whether they performed in good faith their initial agreement to work together to craft a proposal. But there is no way to measure the good faith of a party that is insisting on its own proposal, or rejecting the other party’s proposal, when there are no bounds to the ultimate agreement that they are supposedly trying to reach. Even if we had a written, executed agreement to work together to reach a teaming agreement and submit an agreed-upon bid to Boeing, the written agreement would be unenforceable because of the indefiniteness of its terms. Thus a written, fully executed joint venture agreement is unenforceable when the most essential part of the venture is yet to be determined. See Pacific Hills Corp. v. Duggan, 199 Cal.App.2d 806, 812, 19 Cal.Rptr. 291, 295 (1962).

It is true that contracts may sometimes be enforceable when they leave a matter to be determined in the future, but “it is a question of degree and may be settled by determining whether the indefinite promise is so essential to the bargain that inability to enforce that promise strictly according to its terms would make unfair the enforcement of the remainder of the agreement.” City of Los Angeles v. Superior Court, 51 Cal.2d 423, 433, 333 P.2d 745, 750 (1959). Here, the matter to be left for future determination is the entire teaming enterprise-the sole goal of the initial agreement to work together. Surely that is far too central to permit enforcement of any preliminary agreement to work together for a future agreement. See, e.g., Alaimo v. Tsunoda, 215 Cal.App.2d 94, 99, 29 Cal.Rptr. 806, 808-09 (1963) (option to purchase real estate with price to be determined later by seller unenforceable); Roberts v. Adams, 164 Cal.App.2d at 315, 330 P.2d at 902 (1958) (option to purchase real estate at specified price “payable as mutually agreed by both parties” unenforceable because of uncertainty of terms of payment). I conclude, therefore, that even we view as a separate contract the initial agreement to work together to create a teaming agreement and a joint bid, it is too indefinite to be enforceable.

Because I conclude that the parties merely agreed to agree in the future, and that no contract resulted, I would affirm the district court’s dismissal of the promissory estoppel claim as well. As the majority opinion concedes, the district court’s ruling was correct if there was never any intention to enter a binding contract; promissory estoppel cannot create a contract where none exists. See Rennick v. Option Care, Inc., 77 F.3d 309, 316-17 (9th Cir.1996).”

Just this one last thought – was there ever any intention by the originator to enter into a binding contract… especially considering the pretender lenders that had already sold the loan upstream even before the homeowner signed? As one mortgage broker replied when questioned how they could write mortgages in their own name as lender since they were not a bank, “Oh, we never actually owned the mortgages – Countrywide had already committed and funded the loans before the borrower signed.” Profound, yeah?

Just this one last thought – was there ever any intention by the originator to enter into a binding contract… especially considering the pretender lenders that had already sold the loan upstream even before the homeowner signed? As one mortgage broker replied when questioned how they could write mortgages in their own name as lender since they were not a bank, “Oh, we never actually owned the mortgages – Countrywide had already committed and funded the loans before the borrower signed.” Profound, yeah?

Stay tuned for Part 2 – Dissecting Obligations of Persons Under This Note.

More! More! Outstanding! Thank You.

Question– wasn’t there supposed to be some sort of a document that the borrower-obligor would have to sign which acknowledges that he/she is now made aware of the use of UETA in their matter at hand?

Apparently, there needs to be an explicit agreement in every document at the time it is issued by the obligor (See DC – MERS DEAD DUCKS). If you look on a 1003 Fannie loan application toward the bottom you will see specific verbiage that should have been in all the documents. It appears Mortgage Electronic Registration Systems, Inc. was set-up to skirt UETA’s safe harbor – but apparently it didn’t work and wasn’t explicit enough. I think they made up the “avoiding recordation fees” to hide the actual agenda. Read all of the MERS related posts on DC – especially the most recent.

DC: “I think they made up the “avoiding recordation fees” to hide the actual agenda.”

I couldn’t agree more. MERSCorp had its electronic note registry, complete with its “authoritative copy” m.o. and digital key ready to roll way back. Under the mechanics of their plan, only one party was to have the digital key, that is, the ability to access the digital note. Since only one party was to have that key, what that party accessed with the key’s use was called by MERSCorp the “authoritative copy”. Using this system, no paper copy could exist to compete with the digital ‘authoritative’ copy of the note and under this system, imo, the UCC’s definition – as applicable – of a “holder” takes on a totally new dimension. “Possession” would turn on the one and only party who is supposed to have the digital key. I found and read a lot of their missives about their electronic note registry, but now that I think about it, I don’t recall seeing a couple things, like anything about how anyone was to present the note in litigation, say. “I certify this is a true and correct copy of the electronic / digital note for which only I have the digital key”. It seems to me, though it’s been a few years since I found that stuff and looked at it, that notes were “transferred” by the party with the digital key making an entry in the registry and then the new party somehow having the only digital key. Bookkeeping wise,

the system would show the name of the party with the digital key as the owner of the note. So, essentially, what constituted a transfer of the note was designed, by my take anyway, to actually be the assignment of a new digital key

to the new party, but having nothing to do with any other kind of possession of the note. As far as I could tell and or know, no one oversaw this process. It was strictly voluntarily and wholly dependent on the integrity, long and short, of the members. MersCorp membership rules provided that when a note was sold to a non-member, the member must execute and record an assignment of the deed of trust to the non-member and, briefly, get the loan out of its system. I have no idea how they intended to deal with the loan if that happened since the non-member should get an endorsed paper note, but since a digital note and a paper note may not exist concurrently…..? And then the Consent Order of 2010 or 11 comes to mind.

Did the banks have a loss, or did the banks make a profiteering profit? Show the money trail and the loss on their books Did they get paid over and over by con games, harming my income and causing economic harm and damage to us my deception.

Reblogged this on Justice League.

This is interesting as I have had prob 20 mortgage type loans yet just the one I am dealing with at present from Nov 2005 clearly states at the bottom of the closing docs where the amounts are listed it list 1.Total Paid By/For Borrower -500,000.00 2.Amounts Due From Borrower-350,000.003.Less Amounts Paid For/By Borrower 500,000.004.CASH DUE TO BORROWER 150,000.00 And I have thought since starting this task that it looks to me this is not what one (in common terms)would call a loan. There is 150k to borrower as cash,350k went to pay off old loan=500k so all payments to lender/servicer would should be returned to borrower as their was never a loan.At least not in the conventional sense.

Pingback: PROMISSORY ESTOPPEL: CAN YOU SUE OVER A PROMISE NOT FULFILLED? « San0670's Blog

My note (deed of Trust – in the state of MD) says “the Note…can be sold one or more times…”. Does the word “can” carry the same meaning as “may”?

The question might be “was it” already sold? If I state I can do something when in fact I have already done it and have not disclosed the details – it is disingenuous to say the least. I’m still questioning whether there can be a pivotal agreement concerning something that may or may not have happened that is central to the loan without full disclosure. “Selling” appears to have a different meaning and/or connotation than “securitization” and in some sense securitization is considered more like “leasing” the revenue stream.

The issue appears to be the actual intent of the contract. If the loan was securitized it appears it was not meant to be a traditional mortgage – therefore, did the homeowner and the originator actually have a meeting of the minds?

I have proof mine was pre sold. My servicer used to allow homeowners to print payment history. I closed in January of 2007; first payment was due March 1st 2007. Yet servicer shows my first payment being paid on Dec. 17, 2006. Further, the “originator” filed BK shortly afterwards, declaring in their BK filing that they were a warehouse lender who did not use their own money to fund loans.

johngault, on October 21, 2013 at 8:03 pm said:

No secret mandelman has made a big stink about this blog: my reaction to that ‘stink’:

From the article from attorney Cox at MM ( which does not dispute that paper notes may not be traded electronically btw):

“1. Enforcement of paper notes that are negotiable is controlled exclusively by Article 3 of the Uniform Commercial Code.”

jg: My understanding is that the UCC is default law. Is this to say if Steve and I executed a contract regarding a note wherein I sold it to him, acknowledge receipt of sufficient funds, and handed over the note to Steve – as also acknowledged in our contact – he cannot present our executed contract and the note (not endorsed ever) to evidence his right to enforce the note? Obviously, there is no endorsement, but Steve has a valid contract evidencing a purchase and sale and physical transfer. Why must he turn to default law for his right to enforce?

That’s not a rhetorical question. It’s sincere and deserves an answer. Anyone? Btw, a distinction was being made in the article by the stmt above (Cox): paper notes = UCC III and e-notes = UETA generally. jg: article III = jury not in.

Default law (my words) is that law which is turned to in determining rights of parties generally in the absence of a contract.

“In my five and one half years of representing homeowners in Maine, I have never seen a foreclosure involving an electronic note.”

jg: technically true – we didn’t sign e-notes and DC didn’t say we did. However, Lord knows how many paper copies of electronically stored and / or transmitted notes have made their way thru our courts and foreclosure procedures in the guise of original notes. (Doubting Thomases, take a look at these endorsements on an alleged original note, for example – start at P.16 for endorsements. What possible explanation could exist for endorsement stamps over a borrower’s signature – and the stamps are backward, to boot):

No one, not even DC, posited that these notes were created as e-notes. DC posited, if anything, they were traded as if they had been created as e-notes.

Cox quoting DC (with which he takes major issue):

“Devious planning by the banks schmoozed legislators into passing a law allowing your signature on any document (with very few exceptions) to be transferred electronically.”

jg: I think DC just accidentally inverted some words of her opinion. Think what was meant is “Devious planning………allowing **any document with your signature** to be transferred electronically. DC apparently is not a proponent of e-notes or any other document being transferred electronically.

Cox quoting DC:

“While online agreements cover a good deal of Internet activity; promissory notes, however are viewed bit differently. Even if it was downloaded from the Internet – UETA still mandates that an explicit agreement be made at the time of issuance…”

jg: when I read this, as I recall, more material at DC addressed this further, with the conclusion being that notemaker had to agree the e-note could be transferred electroncially and thus, to me, attorney Cox’s scathing attack doesn’t address what DC actually said, which IF i got it right, appears factual: a borrower must agree an e-note may be transferred electronically. IS this a fact? It appeared so from other material I read.

All in all, the second biggest blunder was to say only e-notes could be securitized if that’s not true and got me, though Cox makes a persuasive case. The first may have been suggesting notes aren’t enforceable for a lack of meeting of the minds **for the reasons for that failure posited therein.**. But if there were a fatal failure of the meeting of the minds as to these notes, I’d say Cox is correct in his statement that it wasn’t cited by DC, whom I’d have to concede as written bases this partly on the intention of the lender to do x,y,z..

Because DC appears to be a firm believer these notes were traded, if at all, electronically, she may have the last laugh even though by this particular article, which admittedly doesn’t represent the quality of most of her work imo, one couldn’t predict it. MERS, MERSCorp, that gang, has in fact created an e-registry and they didn’t do it yesterday. Did they use it to try to electronically trade notes as e-notes which weren’t e-notes, which is at least part of what I think DC really believes? Jury’s still out.

Mandelman must have been pretty annoyed to invite this public critique instead of emailing this hard-fighting author and suggest she straighten it out. Though I have great respect for Mr. Cox, this was blistering and even if this were misinformation, I don’t believe she deserved to get severely skewered publicly.

MM said he didn’t want to take on the UCC (and that’s a systemic problem on our side – none of us do – the UCC sucks, in a word), so I guess the public censor was easier. Boo.

Thank you for the support. I agree the attack was uncalled for, it was unprovoked – irrational and manic in nature. I respect good attorneys; however, many do not have the time to research into the depths of intent. Behind this entire turn of the century securitization creation, which actually differs greatly from the original version, are USTPO patents. Many attorneys have a “deer-in-the-headlights” look when discussing these patents. Patents denote new inventions, new creations (these documents were NOT traditional mortgages) – hence, Sheila Bair calling these NTMs (nontraditional mortgages) throughout her new book BULL BY THE HORNS.

These patents cover every aspect of securitization, NTMs, subprime mortgages, foreclosures, REOs and all one has to do is dig and comprehend with good recall what they are reading. If you can’t handicap a thoroughbred horse race you probably should not be a foreclosure defense attorney. There are researchers more qualified than I am who have jumped into the patent rabbit hole and linked more than any of us want to know.

In our research we have found patents that describe in detail how an Article 3 negotiable instrument can manifest into Article 9 securities transaction. One such patent has been posted several times on DC: https://deadlyclear.files.wordpress.com/2013/04/patent-ep1376311b1-system-and-method-for-creating-vaulting-transferring-and-controlling.pdf. We’ve spoken directly to the patent creators (which I doubt many attorneys have taken the time to do) in order to understand how these patents were used and their prime intention at the time they were created – and who hired them to write the patents and design.

Just reading that one patent alone is not enough to link the information; however – we have read numerous patents, pulled hundreds of documents out of the failing banks’ bankruptcies, as well as exhibits, affidavits, and depositions out of the investor and bank related lawsuits… like I said your knowledge level and ability to have decent recall (like remembering the bloodlines and racing patterns of a good thoroughbred) is essential in order to connect the dots.

Our in-depth research tell us that it appears the NEW turn of the century securitization was intended to be electronically transferable. The intention started in the 1980s and developed out in the early 1990s and is still continuing today. That was one of the reasons (if not the primary) for Mortgage Electronic Registration Systems, Inc. and just the bi-line trade name in the mortgage really wasn’t enough to overcome the “safe harbor” provision in the UETA and E-sign statutes as MERSCORP, Inc. claimed was its intention to do. See: https://deadlyclear.wordpress.com/2013/09/27/the-history-and-death-of-mortgage-electronic-registration-systems-inc-according-to-the-ustpo/ and click on the #10 exhibit: July 16, 2007, MERSCORP, Inc. files more advertising specimens with the USTPO. [Click HERE for Exhibit “H”]. Go to page 12 and read the MERSCORP propaganda – this was filed by MERSCORP, Inc. in the USTPO and the document was created in 2003 or before (what is filed in the USTPO as a specimen is supposed to establish the use of the trademark over the preceding years). MERS® was considered an “eRegistry” – well, how in the hell do you think you get a document into an eRegistry unless you are an electronically transferable document? Duh!

This goes to the heart of the concept of the post which was to stimulate the thought process, not to practice law or challenge retired attorneys and bloggers. This research was meant to be considered with previously documented material in earlier posts (as you suggested) – that if they hadn’t read or retained – they might not be able to connect the dots.

Does this new turn-of-the-century securitization actually work? Given all of the lawsuits, the discrepancies and failures to follow law and procedure – it would seem obvious to question the nature and actual intent of the documents, wouldn’t it?

Finally, the only reason to attack a foreclosure defense warrior is to try and destroy them – and if you are on the same team you try to glean and share information. Fortunately, DC readers, foreclosure defense attorneys and homeowners are more intelligent than was suggested by the attacks (and there are more of us than attackers). Everyone is entitled to an opinion but attacking out of nowhere is nuts. This isn’t a competition or war game unless you are on the other side and certainly none of us on the foreclosure defense side are cashing checks from the banks. In the case of the bloggers and the retired attorney (who BTW it appears openly admits he had a thriving business at one time working with the FDIC and the banks) – I leave it for the the public to decide. We provide the research and information for the public to better access.

There are several dozen of us that research, read, review these documents and interview the creators of this material. If you don’t bother to read the documents or follow the DC blog – you may miss a step (which we try to reiterate but don’t always catch); but you have to open up the links and READ the documents – knowledge doesn’t come from osmosis. The research is meant to stimulate the curiosity, empower with more knowledge and dig a little deeper behind the securitization curtain to expose the Oz.

The misconception or misunderstanding that the eNotes are traded in the new securitization process – appears to be incorrect. But one must read the patent that was posted (and others) along with other posts to understand that the mortgage loans were to become static or passive (locked in a vault) after they were bundled for the trusts and certificates were created from the revenue and issued for trading purposes. That is how an Article 3 negotiable instrument that becomes static and morphs into an Article 9 securities. However, it would appear obvious that in order to enter the MERS® “eRegistry” the documents would need to be electronically transferable… not to mention how they got to Wall Street from all over the country.

MERS. We all certainly have our opinions, don’t we? Naybobs may add this one to the fodder: MERS was created, in part, to handle the fact that these trusts may not own real estate (and certainly not after a closing date), which would be the result of a successful credit bid by a trust (as if) at a foreclosure sale. MERS was designated the ‘nominee’ as well as beneficiary instead of the ‘agent’ to willfully bifurcate the note and deed of trust to that end – MERS would be a NON-agent in order to hold that real property, as agency would implicate ownership by the trust. One might give this some thought before disregarding…….

http://stopforeclosurefraud.com/2013/11/11/bombshell-us-bank-admits-the-borrower-is-a-party-to-an-mbs-transaction-that-securitization-trustees-are-not-involved-in-the-foreclosure-process/

Pingback: Policy Changes aka eNotes are Here! New Paragraph 11 in Promissory Notes. | Deadly Clear

Reblogged this on Deadly Clear and commented:

The more we advance information – the more relevant earlier posts become.

Reblogged this on AXJ USA NEWS and commented:

AXJ CLASS ACTION AGAINST GREEN TREE SERVICING CLAIMS IT DOES NOT OWN NOTES AND HAS ROBO-SIGNED THOUSANDS OF DEEDS OF TRUST,

I’ve tried this tack about 30 times in my litigation, and each time the judge ruled against my clients without reaching the argument…in other words, the judge will always find a different reason to rule in favor of the bank and will never discuss the issue…

More often than not it appears the lower courts have been told to rule in favor of the banks and if the homeowner can afford to appeal – maybe they’ll get justice at that level. The only reasonable answer for this, IMHO, is that they are all so highly invested in Wall Street, whether in mutual funds, pensions and/or stocks that they are afraid if the banks can’t remain liquid by processing the foreclosures they may fail – and there goes retirement. Since 2010 it appears the federal court judges have divested their bank stocks – but I see a lot of lower court judges (foreclosure) that still have risky investments like PIMCO who had been buying MBS and had a sweet deal profiting from the FED. However, in 2014 things changed and PIMCO began to have internal issues and pulled back from its MBS shopping spree. See http://www.housingwire.com/articles/29277-pimco-cuts-mortgage-backed-securities-holdings Nevertheless, judges don’t always have the time to follow the trends and listen more to advisers.

We’re pushing the pre-existing investment bank agreements to procure collateral for the purpose and intent of securitization (securities sales) under the guise of a traditional looking mortgage and note documents. We have the pre-existing agreements and there are already admissions that these were NTMs (non-traditional mortgages). How far we can get is anybody’s guess.

Yes, I now agree that judges will bend over backwards to give “lenders” the verdict. And the judges who do will continue to do so – as long as they don’t fear appeal to the very top. Safe bet since most homeowners can’t finance such a mission.

I don’t know how that electronic note registry was supposed to be consistant with another MersCorp’ rule from the early days. In order to foreclose in Mers’ name, the member had dto have possession of the note (and they didn’t speak in this mandate, to my knowledge, about endorsements, just possession!). Since MERS already showed in public record, guess they thought this “possession” of the note and MERS being in the dot = unity. If MERSCorp found that the party foreclosing in Mers’ name didn’t have the note and foreclosed, the member was subject to a 10,000.00 fine…..to MERSCorp! Heck with the homeowner! The member wasn’t obligated by the terms of the membership agreement to set right the improper foreclosure!) But, what I mean is…..what?! For this unity, “Mers” was to be made the party with the digital key? I was always hoping to try to see that gang nailed for their stories in Nebraska Dept of Banking v MersCorp (or mers, I forget) since they swore mers had no interest in notes in order to defeat Nebraska’s licensing requirements.

Pingback: Paul Krugman Propaganda Fully Exposed and Debunked | Deadly Clear

Pingback: Securities Fraud: In Search of the Holy Grail of Foreclosure Defense | Deadly Clear

Pingback: About Those PSA Signatures | Deadly Clear

Pingback: AMERICAN HOMEOWNERS: CALL FOR A MORATORIUM ON ALL FORECLOSURES IN 2019! | Deadly Clear

What I find truly remarkable are the 50 state AGs, the OCC, FTC, and CFPB that failed to mandate the removal of the fraudulent assignments and documents in the land records office. The weeny National Mortgage Settlement was nothing but a slush fund transaction. Had these agencies mandated that the banks, trustees & servicers physically remove these documents or be fined daily – and followed through to substantiate the removal of falsified documents – the “Settlement” might have had some teeth and been worthwhile.

Pingback: The American Dream of Homeownership is under Attack | Deadly Clear