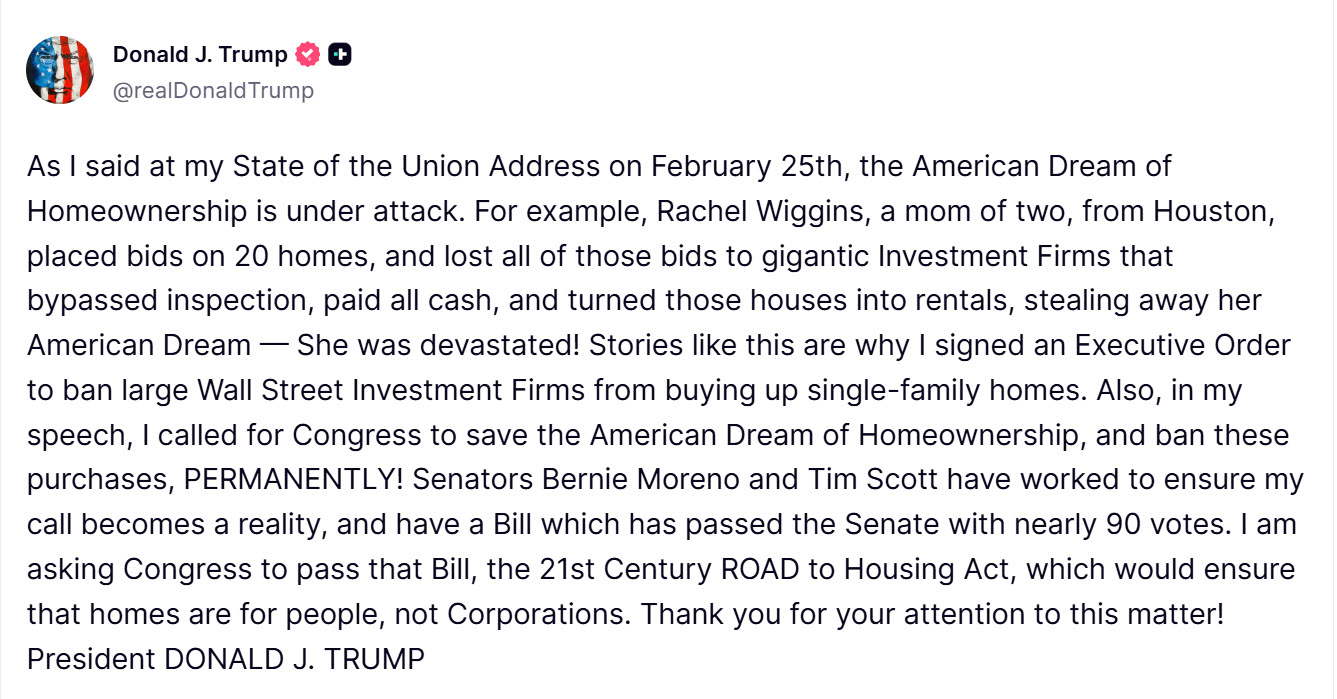

And has been for several decades. A Truth Social post 5/11/2026:

The attack on the American Homeowner relates directly to the attack on pension funds all across the country (and even around the world). Pension deficits and mortgage fraud are synonymous with the largest securitization Ponzi scheme ever to have existed in America. Former FDIC Chair Sheila Bair said it best, these fraudulent financial products were not traditional mortgages, they were NTMs – “Non-Traditional Mortgages” – and they faked out the entire mortgage industry. It’s time for a Letter to President Trump.

Dear President Trump,

We too are stressed out about the number of foreclosures and most of what we see contain fraud. Whether its fabricated declarations, accounting errors, inflated figures or judges failing to follow the rule of law – it’s out of hand and has been for years. We are writing to respectfully request that you consider a temporary federal moratorium on residential foreclosures until after the upcoming midterm elections, to allow Congress time to examine and address unresolved issues surrounding mortgage securitization and foreclosure enforcement.

Moratoriums are the only action that seemed to make banks slow down and negotiate with homeowners. Right now, banks are just trying to get the debt, bad paper and fraudulent financial products off of their books because they wrote more loans than they can legally hold. And investors, as

well as Fannie Mae, have tossed many of these loans back to the servicers.

Many homeowners entered into what they reasonably understood to be traditional mortgage transactions. In practice, a large percentage of these loans were originated for immediate securitization, transferred through complex trust structures, and enforced years later by parties whose legal authority is often unclear even to experienced judges; and certainly to inexperienced attorneys (the system has eliminated many of the knowledgeable attorneys). This has created widespread confusion, inconsistent rulings, and growing public distrust in the fairness of the mortgage and foreclosure process.

State legislatures and lower courts are not well equipped to analyze securitized trust documents, pooling and servicing agreements, or the distinction between loan ownership, servicing rights, and enforcement authority. Many attorneys lack the necessary IQ and history needed to adequately defend their clients. Let’s face it, securitization wasn’t taught in law school and reading through a securitization prospectus is about as exciting as reading a Podunk telephone book. As a result, similarly situated homeowners often receive radically different outcomes depending on jurisdiction, judicial familiarity, or access to expert counsel.

A temporary moratorium would not cancel debts or forgive obligations – albeit, the thought of a Jubilee to dump the fraudulent paperwork isn’t an all bad idea. Rather, it would preserve the status quo while Congress conducts hearings, reviews existing law, and determines whether clearer national standards are needed to ensure that homeowners are not unknowingly deprived of property by entities that cannot demonstrate a lawful right to enforce. Even when the bank run’s outside of the statute of limitations or has faced one or more “dismissed with prejudice” court orders – they will judicial shop until they find a judge that will play on their team – even if the decision isn’t lawful, because they know a good majority of the foreclosure legal counsel that remains is lazy or just not knowledgeable about securitization and rehypothecation.

We’ve even had a judge express his disdain for any homeowner that tries to bring up securitization issues in his court.

Foreclosures carried out under legal uncertainty harm not only families, but also communities, land records, and confidence in the financial system.

Pausing this process briefly, while elected representatives evaluate appropriate reforms, would demonstrate prudence, fairness, and respect for due process.

We respectfully ask that you consider using your executive authority to implement a limited foreclosure moratorium, narrowly tailored in scope and duration, to prevent irreversible harm until and while Congress addresses these issues.

Thank you for your time and consideration.

Respectfully,

The DeadlyClear Editorial Staff