Good information sometimes bears repeating.

The over-burdened judiciary isn’t always up to speed as quickly as it ought to be and good case law doesn’t always make it to the top of the pile for the clerks to review and digest. Even good attorneys occasionally miss pertinent material.

The over-burdened judiciary isn’t always up to speed as quickly as it ought to be and good case law doesn’t always make it to the top of the pile for the clerks to review and digest. Even good attorneys occasionally miss pertinent material.

So, let’s go back to about 2 years ago when Yves Smith, who is an absolutely brilliant author and blogger of “NakedCapitalism” and 4closureFraud, truly a leader in the foreclosure defense blogging pack, wrote about an Alabama securitization case named U.S. BANK v. ERICA CONGRESS.

Of course the case went to appeal and the outcome of the appellate decision was a unanimous decision, the Alabama Court of Civil Appeals reversed a lower court decision on a foreclosure case, U.S. Bank v. Congress and remanded the case to trial court. The reasons hinged upon 2 superb expert witnesses. The Alabama Court of Civil Appeals opined:

“Congress challenged that evidence by presenting the testimony of Thomas J. Adams, an expert in mortgage securitization, who stated that the fact that the allonge was physically located in a different part of the custodial file indicated to him that it had been created at a later time. In addition, as the trial court noted in its judgment, there was some confusion regarding where the custodial file was actually kept pending GMAC’s request for the file, which, the trial court stated, at least indicated “an opportunity for the documents to be altered or manipulated.”

Thomas J. Adams was partner with the firm of Paykin, Krieg & Adams in New York and his expertise is in the field of securitization. Reading Mr. Adams’ affidavit along with another expert used by Ms. Congress, Professor Ira Mark Bloom, who was employed as the Justice David Josiah Brewer Distinguished Professor of Law at the Albany Law School in Albany, New York begins dissecting the characterizations of what constitutes the legal entry into a securitized trust.

Thomas J. Adams was partner with the firm of Paykin, Krieg & Adams in New York and his expertise is in the field of securitization. Reading Mr. Adams’ affidavit along with another expert used by Ms. Congress, Professor Ira Mark Bloom, who was employed as the Justice David Josiah Brewer Distinguished Professor of Law at the Albany Law School in Albany, New York begins dissecting the characterizations of what constitutes the legal entry into a securitized trust.

Professor Bloom’s area of expertise is in the law of Trusts, Property, Estates, and Taxation with an emphasis on New York law. Are you in love yet? Professor Bloom states in his affidavit starting at paragraph 7:

Professor Bloom’s area of expertise is in the law of Trusts, Property, Estates, and Taxation with an emphasis on New York law. Are you in love yet? Professor Bloom states in his affidavit starting at paragraph 7:

“7. In formulating my opinion, I have relied upon applicable New York law because Section 11.04 of the trust agreement, which is called a Pooling and Servicing Agreement (PSA) and under which plaintiff purports to be Trustee, provides in applicable part that the trust agreement “shall be governed by and controlled in accordance with the laws of the State of New York …”

8. In formulating my opinion, I have been guided by the following trust and property law rules under New York law:

A. Unless an asset is transferred into a lifetime trust, the asset does not become trust property. (NY Estates, Powers and Trusts Law § 7-1.18).

B. The assignment of a mortgage without transfer of the underlying promissory note is a nullity. (Merritt v Bartholick, 36 N.Y 44 (1867); Kluge v. Fugazy, 145 A.D. 2d 537 (1988)).

C. A trustee’s act that is contrary to the trust agreement is void. (NY Estates, Powers and Trusts Law § 7-2-4).”

Two years ago, many judges had no clue about securitization; and, outside of New York – dealing in NY trust law would be like counting money in a foreign country. The judges weren’t alone. Attorneys had trouble handicapping this race horse too. NakedCapitalism gets into the meat of the matter and tears apart the Deutsche Bank’s argument against the comments from another well known Georgetown University law professor, Adam Levitin.

NakedCapitalism comments on the Deutsche diatribe:

“This is simultaneously laughable and damaging. The argument basically boils down to: “Gee, the fact that no one bothered to observe the contracts means they never intended to. So we’ll just pretend those provisions don’t count.” Does that mean that people who promptly went into default obviously never intended to pay, and should therefore get free houses? Or that when a borrower sends a payment a day or two late, they clearly intended to pay on time, so no late fees should apply? I think a lot of people would agree to that theory of contracts as long as it applied to consumers as well as banks.

“This is simultaneously laughable and damaging. The argument basically boils down to: “Gee, the fact that no one bothered to observe the contracts means they never intended to. So we’ll just pretend those provisions don’t count.” Does that mean that people who promptly went into default obviously never intended to pay, and should therefore get free houses? Or that when a borrower sends a payment a day or two late, they clearly intended to pay on time, so no late fees should apply? I think a lot of people would agree to that theory of contracts as long as it applied to consumers as well as banks.

But notice the amazing admission: “then to have systematically failed to observe those expanded requirements.” This is even better than Kemp v. Countrywide! The head of the ASF tells the public in Congressional testimony that the entire industry group he represents “systematically failed” to honor their own agreements!”

And they got bailed out with BILLION$ in TARP funds for their failures. Let’s think about this for a moment from a different perspective – premeditation (which we all know at some level there had to have been a plan because not EVERYBODY fails to assign the mortgages by accident or mistake). Mr. Adams states in paragraph 22:

And they got bailed out with BILLION$ in TARP funds for their failures. Let’s think about this for a moment from a different perspective – premeditation (which we all know at some level there had to have been a plan because not EVERYBODY fails to assign the mortgages by accident or mistake). Mr. Adams states in paragraph 22:

22. Based upon the information provided to me and the documents that I have reviewed I can state that the allegation that the Trust obtained this promissory note on July 29, 2008 would violate the REMIC provisions of the IRS tax code for a number of reasons. First, the loan was in default on July 29, 2008. Therefore the loan could not have been a “qualified mortgage loan” under the IRS tax code because a qualified mortgage loan is a performing mortgage loan…

Here we are again, the REMIC Has Failed! However, what if the loan was not actually in default? Well, 2 years later and after reviewing hundreds of Pooling and Servicing Agreements (“PSA”), the thought crossed our minds that maybe the loans were not actually shown to be in default because maybe Mr. TARP was paying off the tranches?

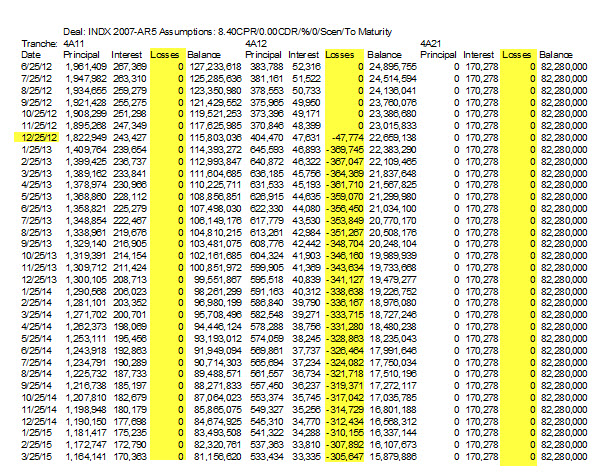

In the trust tranche detail excel spreadsheets we’ve examined – losses don’t start showing up until late 2010, if at all [Ed. note: some losses may have occurred earlier but those examined in our batch appeared to have been paid – by someone]. An example of a partial trust excel report for INDX 2007-AR5, 3 tranches (4A11, 4A12, 4A21) show no losses. Only 4A12 begins to show a loss on December 25, 2012. Merry Christmas.

Even more interesting when reviewing trust tranche detail, for example, in the INDX 2007-AR5 there are 12 of the 19 tranches that pave been paid off (see the grey areas) – again by whom and how? Unknown info, but thank you very much.

Even more interesting when reviewing trust tranche detail, for example, in the INDX 2007-AR5 there are 12 of the 19 tranches that pave been paid off (see the grey areas) – again by whom and how? Unknown info, but thank you very much.

Knowing where your loan is, of course is extremely important. Getting your information before the trust winds down is even more important – even if you are not facing foreclosure.

Knowing where your loan is, of course is extremely important. Getting your information before the trust winds down is even more important – even if you are not facing foreclosure.

What do we do with this information? Hypothetically, let’s think about this. What “if” there are contracts and agreements by other guarantors or surety(s) that the borrow is not privy to, and didn’t agree to reimburse? There is a paragraph in most Promissory Notes that has never been dissected – or at least not very well:

The TARP bailout was due to an economic force majeure caused by Wall Street corruption that did not stem from homeowners failing to make payments. It was a much bigger Ponzi scheme than that and we have to face the fact that these crooks were the King of CYA – so would it be surprising that someone would underwrite your obligation without your knowledge? Do you owe someone who gives you a gift? If Grandma (or your Sugar Daddy) makes your mortgage payments and you have no contract of repayment – is it legally paid? The IRS says as long as neither you or your Grandma (or Sugar Daddy) claim a deduction – they have no problem with it.

And frankly, how would you ever know that the bank hadn’t transferred and assigned the notes properly? Many people didn’t, they just couldn’t get a timely refinance – even with good credit because the banks could not perform… long before the borrowers fell into default.

Where is the moral hazard here? The homeowners could have refinanced if the Wall Street banksters had made legitimate mortgages… but they didn’t. Any investor lawsuit will tell you that the banks inflated the appraisals, systematically abandoned the underwriting guidelines and purposely over-rated the bonds. This was not the fault of the homeowner.

Reading Neil Barofsky’s BAILOUT links the thought process with the fact that HAMP was designed to “foam the runway” for the banks, not bailout the homeowners. So, were TARP funds used to prop up the insurance companies and pay off the tranches and keep the loans current?

Reading Neil Barofsky’s BAILOUT links the thought process with the fact that HAMP was designed to “foam the runway” for the banks, not bailout the homeowners. So, were TARP funds used to prop up the insurance companies and pay off the tranches and keep the loans current?

And why would they want to do that? Maybe to keep even more investors from suing or to make some payments and negotiate settlements with investors while the banks tended to their fraudulent foreclosure process? NakedCapitalism questions the “continued timidity” of investors to confront the fraudulent assignment issue:

“Nevertheless, it’s possible no investor will decide to pursue this sort of case, which would leave this question unsettled (trustees are apparently threatening investors not to, and I am told a lot of buy side investors are loath to alienate the dealer firms on which they think they depend for information. But there are some major actors, like Wells Fargo and US Bank who would seem not terribly well positioned to retaliate even if these concerns were valid). However, consumer lawyers are getting more and more sophisticated in using the PSA arguments to fight foreclosures, and the more bad press the banks have gotten, the more receptive judges appear to be becoming.”

Well, its 2 years later and more judges are listening to these arguments and on the heels of understanding the fraudulent assignments comes along the rigged LIBOR rates – ANOTHER FRAUD UPON THE HOMEOWNER. It’s certainly time to level the playing field. Maybe this securitized trust information, for example, can be used in arguendo –

“Your honor, the Plaintiff Trustee before you represents a trust that alleges my client’s loan belongs to. Although we believe the Plaintiff has unclean hands in this court of equity, we would like the court to compel the Trustee to provide the spreadsheets from the Trust that is actively trading and indicate the tranche(s) my client’s loan is alleged to have participated in; and should the court find that at the time of the foreclosure, my client’s loan tranche(s) are found to be current, we respectfully submit that the Court dismiss the Plaintiff’s action with prejudice.”

“Your honor, the Plaintiff Trustee before you represents a trust that alleges my client’s loan belongs to. Although we believe the Plaintiff has unclean hands in this court of equity, we would like the court to compel the Trustee to provide the spreadsheets from the Trust that is actively trading and indicate the tranche(s) my client’s loan is alleged to have participated in; and should the court find that at the time of the foreclosure, my client’s loan tranche(s) are found to be current, we respectfully submit that the Court dismiss the Plaintiff’s action with prejudice.”

So, what’s it going to be for these banks – copping to falsifying Bloomberg Terminal and SEC records and fabricating statements provided to the investors’ management – who don’t want to know the ugly truth because they’d have to tell all the retirement and pension fund employees about the loss and the fraud?

So, what’s it going to be for these banks – copping to falsifying Bloomberg Terminal and SEC records and fabricating statements provided to the investors’ management – who don’t want to know the ugly truth because they’d have to tell all the retirement and pension fund employees about the loss and the fraud?

Yup, that’s why investors aren’t screaming about the lack of proper assignments – at the homeowner’s expense… and this is where the rest of the moral hazard is hidden.

Are you getting the big picture, yet?

So– what else is new? I’ve been saying it for years. Both federal and state judges’ retirement plans hold investments in MBS and bank stocks. As do other federal and state employees, including FBI agents, district attorneys, sheriffs and even county court clerks!

Then we have the State Attorney Generals who sold out without any investigations by signing on for settlement.

Clearly nothing will change.

In California– the Superior Court judges do not even care about securitization.

They will only hear someone is in default thus the non-judicial foreclosure stands.

This is certainly true, but won’t they be surprised when they go to retire and nothing is there… Or very limited…karma.

But how do you figure that nothing or very little will be ‘there’ in the retirement pensions?

Clearly TARP may be being used to continue the payments to investors but so is all the monies obtained from insuring on the defaulted loans!

Remember, they CYA by insuring between 15 and 30+ times the full mortgage loan amount (what loan payments would be after 30years). That is huge….and could easily allow them to continue to pay monthly amounts to investors and still make profits. PLUS, when they got the insurance monies from the ‘defaulted loans’– the banks can invest most of those insurance monies and make even more money on the backs of the unsuspecting homeowner-borrowers.

The lure and appeal of getting the insurance proceeds even resulted in the banks placing some homeowners into a ‘false default’ state. Even the forced place insurance that banks use to place a homeowner into default on the mortgage is another way the bank can collect on their ‘bet’ that the homeowner will default.

Washington DC has really done nothing to investigate, nor will they.

There was no interest about any of this during the election.

It’s Monopoy’s ‘get out of jail’ free card.

If you watched Ann Curry’s story last night on NBC Rock Center, you would have heard that the USA has over 1 million HOMELESS school age children!! She focused on the new middle class homeless. Many have college degrees and even advanced graduate degrees.

It’s a tragedy for Main Street Americans and we are bombarded with diversion news stories– like Paula & Petreaus, the twins from

Florida who tilt their heads at the same angle, the shirtless FBI agent etc.

I must say though that I enjoyed the news story & video about the white pony and the zebra who escaped and ran thru the streets of NY this week.

Economists say $600 TRILLION was gambled and there is no way they can “fix” that. Look at the union busting..look at Hostess Brands, just an example of the damage yet to come. The money is gone. Anyone with a 401k or mutual funds still sitting out there might as well roll the dice on a crap table. Millions have already lost their pensions or had to use them out of necessity. Smart guys have cashed in and got out… They know first come, first served -and there’s not enough to go around. It’s just a matter of time.

Abby, I have been trying to get in contact with you. Please contact me, Marina in Santa Barbara CA marina333sb@yahoo.com

Great article Virginia! One of your better ones, and you’ve had several. Mahalo!

the cartel is in full command of the judiciary…and the law is only applied to you…best move was the one in 1776…to break the cartel stranglehold…sad…

actually we found out today a loan that was sold one 503 times

Was this Fannie Mae or Freddie Mac?

Who sold it 503 times?

Re: $600 trillion

Perhaps they are still trying to prop up pensions cause on sept. 13th they announced the Fed would be buying $40billion per month (that is a ‘b’) of MBS!

FRAUD IS FRAUD THIS MESS IS PULLING DOWN THE ENTIRE AMERICAN JUSTICE SYSTEM AND DESTROYING THE BASIC PREMISES ON WHICH THIS COUNTRY FUNCTIONS. THERE NEEDS TO BE AN ALL OUT FRONTAL ASSAULT AND EXPOSURE OF THESE MODERN DAY JOHN DILLINGERS. WE MUST EDUCATE AND THEN DEMAND THAT THESE JUDGES RULE BASED ON LAW RATHER THAN MIGHT OR THEIR OWN VESTED INTEREST.

Great article!

Iceland had it right.! ! ! ! They locked up the Banksters and now after a few short painful years are doing very well as a country. Americans should study or even just pay attention to history. As these “wonderful Hedge Funds” are going to buy up all these houses and rent them out. And then to cover their criminal activity they will create securitized assets of the rents and investment vehicles/ chop them up and sell them off like they did with the mortgages.

Totally agree with Daniel.. America should have led the way and still haven’t followed the good example of Iceland. 🙂

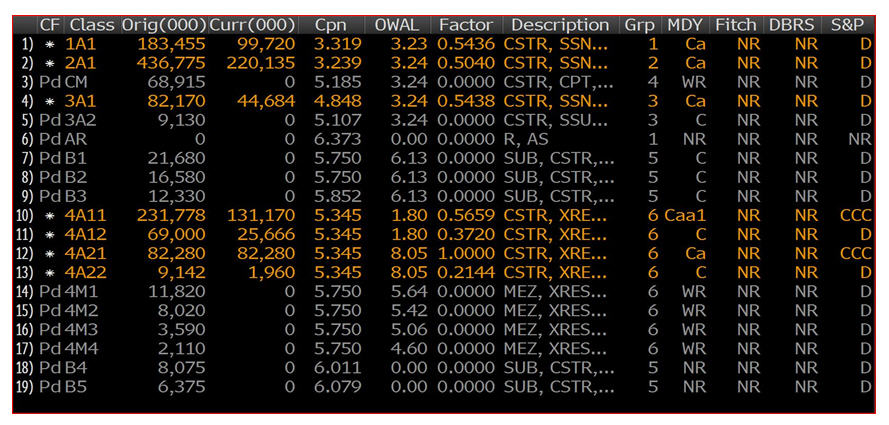

It appears that the figures in the chart are assumptions. It says “Assumptions.”

When I crunch any of the numbers associated with tranche 4A12 after 12/25/12 I don’t find that any of them rectify.

This is how they are handled on Bloomberg – they assume they’ll have losses – maybe? Interesting, yeah?

It’s just too bad that Ms. Webber bans people who don’t agree with her, she “suspects of having an agenda” or flat out tell her that she’s wrong. It was only about 3 years ago that she did an incredible 180* and suddenly believed that servicers were participating in Mortgage Servicing Fraud and that the industry was as bad as people were telling here it was…

Abby, brilliant as usual. Am going to court Friday to stop BOA from selling our home illegally online, though they have no legal title. There have been four warrants signed by the LTC judge, but BONY never evicted. Four warrants before the sheriff finally served? We finally did win on appeal though. Brutal, the corruption from the lawyers alone.

But it all starts here… http://www.ritholtz.com/blog/2011/12/fbi-estimates-80-of-mortgage-fraud-involved-industry-insiders/

The U.S. Treasury’s Office of Thrift Supervision noted last year (page 7):

“The FBI estimates that 80 percent of all mortgage fraud involves collaboration

or collusion by industry insiders.”

THE WHOLE COLLAPSE WAS A RICO PONZI SCHEME DESIGNED TO STEAL THE EQUITY OF MILLIONS OF PROPERTIES!

And we lead the way! Bill Paatalo Investigative Agency. Feel free to contact us about your litigation. We love chatting with your (qualified) attorneys….

-Rob Harrington/ National Mktg & Case Intake Manager

STEP 1- FREE SECURITIZATION LOOK-UP LINK >>> https://bpia.wufoo.com/forms/free-securitization-check-courtesyrob-harrington/

Reblogged this on sandrakblog and commented:

please read this