Regarding the 2020 Foreclosure & Eviction Moratorium

By Sydney Sullivan

For nearly a dozen years, we have followed the securitization/rehypothecation crisis and corruption on behalf of over 200 million American Homeowners (2.5 per HH) and their families. It’s been a tough 12 years and some families are still fighting fraudulent bank foreclosures since 2009. Can you even imagine a lawsuit and the threat of losing your home for over a decade, waking up every morning wondering when the sheriff is coming to throw you, your family and your belongings out on the street?

Thank you in advance for considering our plight. We applaud your “Moratorium” on evictions and foreclosures and the extension which you added just this week – but Sirs, it’s very limited. It doesn’t reach a lot of people that are in dire need and let us tell you why.

Your moratorium is limited to FHA loans. It should be open to all homeowners with mortgages after 2002 (if not before) given the depth of corruption in the industry. Most of the loans started off “originally” in the newer (circa 2000) ramped up version of securitization/rehypothecation as FHA, or GSE (Government Sponsored Enterprises – Fannie & Freddie) backed loans. Now, we all know that GSEs weren’t really the government, nevertheless securitization at the turn of the century was designed and patented for fraud and foreclosure – unbeknownst to most Americans.

Legislators and Judges were spoiled rancid by their retirement portfolio investments that were filled with Mortgage-Backed Securities (MBS) – an obvious appearance of impropriety and conflict that was ignored. Smear campaigns had filled the fake news airwaves that homeowners were irresponsible and “bought more than they could afford” when in reality the American homeowners were sold mortgages like stock shares. Mortgages were given on what the borrower would agree to pay and appraisals were intentionally inflated to meet the value needed for the banks and ultimately – Fannie Mae.

Fannie even patented the process of “willingness to pay” versus actual real estate value. Of course, the sales pitch to the homeowner was, “your house is appraised at $600,000 so you can refinance and pull out $200,000 and buy a second home” (or a boat, or take a trip, send the kids to college – whatever the kicker was to hook the fish). “Land prices have always escalated for the last 70 years,” another bankster narrative.

Wall Street Wolfs were everywhere – your neighbors, relatives, lodge brothers, church members – all people you thought you could trust. And frankly, they probably had no idea what these bank executives and financiers were doing in their ivory towers or the overall intent.

The Wolfs were only in it to make money and the paperwork was sloppy, if not in some cases, criminally forged.

These loans were not traditional mortgages. As Sheila Bair (former FDIC chair and author of Bull By The Horns) called them – they were NTMs. Non-Traditional Mortgages. There was nothing “traditional” about these loans. They were abusive, patented foreclosure software for scams (the intent is in the USPTO patents) that should never have fallen under the state and federal statutes of a traditional mortgage because they were anything but. These were securities before the homeowners ever signed the faux documents. The procedure was designed to trash the Chain of Title.

But let’s get back to your moratorium for “FHA loans.”

It appears that a great majority of loans started out as GSE guarantees. However, the GSEs participated in a nationwide predatory mortgage lending scheme, a complex confidence game that led the Department of Justice (“DOJ”) to file suit against Bank of America, et. al., its former (Countrywide) and current subsidiaries and partners, on October 24, 2012. Due to the nature of the DOJ case, documents were originally sealed, some were released though many remain sealed today.

The overall DOJ case did not completely resolve until May 23, 2016. The case publicly unleashed the secret that subprime loans by large mortgage companies such as Countrywide and New Century Mortgage Corporation (“NC”) sold and pledged their

procured loans to Fannie Mae and Freddie Mac.

“Fannie Mae and Freddie Mac purchase single-family residential mortgages from lenders” (Intervenor Complaint, ¶18). “GSEs buy single-family mortgages from mortgage companies and other financial institutions [. . .] then either hold the loans in their investment portfolios or bundle them into mortgage-backed securities (“MBS”) that they sell to investors.” (Intervenor Complaint, ¶27)”

USA v. BofA, et. al., USDC Southern District of NY, 12 Civ. 1422 (JSR) (Oct. 2012), Complaint-In-Intervention of the USA (“Intervenor Complaint”).

During this period, numerous other governmental agencies filed suits relating to the mortgage crisis. Until their resolutions were recently made public, it was impossible for American Homeowners to adequately defend against the judicial foreclosure and sale process. As government related lawsuits and consent orders evolved it established the intentional cover up of countless frauds against homeowners in an ongoing pattern of complicity.

Homeowner “mortgage” loans were primarily sold by a local brokers through large subprime companies like New Century and Countrywide to Federal National Mortgage Association (“Fannie”), who was a facilitator of securitized loans with its own securitization pools that were deliberately impossible to find; intentionally not listed in the Securities and Exchange Commission (“SEC”) and even hidden on Bloomberg Terminal.

Fannie’s involvement began in the overall scheme started before the turn-of-the century and became paramount with the use of Fannie patented software “1003 loan application process.” However, from the inception of loans primarily after 2003, FANNIE’S ROLE WAS INTENTIONALLY CONCEALED. Pursuant to Fannie’s 2008 Servicing Guidelines:

“Fannie Mae is at all times the owner of the mortgage note, whether the note is in Fannie Mae’s portfolio or whether owned as trustee, for example, as trustee for an MBS trust. In addition, Fannie Mae at all times has possession of and is the holder of the mortgage note, except in the limited circumstances expressly described below.”

In March 2007, Fannie severed business ties with New Century. This meant New Century could no longer sell loans to Fannie. This also meant homeowners with New Century loans would have difficulty finding where their loans had traveled. Assignments of Mortgages were only created and filed when the homeowner defaulted. If the homeowner didn’t default and wanted to find his loan, only the original recorded copy of the mortgage existed. New Century thereafter entered into a liquidating trust, New Century TRS Holdings Inc. bankruptcy, Case No. 07-104416 (KJC) on April 2, 2007 – and thus, the great paper shuffle ensued.

In one such case, the homeowner filed a claim in the New Century bankruptcy only to be told that New Century did not own the loan. It had been sold to Lehman Brothers Bank in 2006. That’s where the New Century file stopped. Lehman Brothers Bank had no files on the loan and its parent company, Lehman Brother Holding Company, Inc. had filed bankruptcy in September 2008 (the Great Crash). It too also had no files.

Other than an obviously manufactured fraudulent assignment of mortgage from New Century to a U.S. Bank Trustee in 2009 (well after the NC bankruptcy) crafted without authorization or acknowledgment of the New Century Liquidating Trust Trustee – who, BTW, had already provided the homeowner with an affidavit that New Century had sold the loan to Lehman Brothers Bank in 2006 – the Plaintiff (U.S. Bank) had no other evidence of standing to pursue a foreclosure. The circuit court judge in the foreclosure case ignored all the evidence, including New Century Trustee’s affidavit and New Century’s bankruptcy court clarification in an order as provided in exhibits by the homeowner – and ruled in favor of the bank plaintiff. The case is still on appeal.

“Fannie collaborated with numerous banks to commit identical deception programs” on countless homeowners. Fannie had instituted the relaxed underwriting program in 2006, now known as Expanded Approval (“EA”). This allowed subprime lenders like New Century and Countrywide’s “hustle” to sell riskier loans to Fannie. The Securities and Exchange Commission (SEC) Complaint against the GSE’s executives filed on December 16, 2011 states:

“Fannie Mae did not tell investors that in calculating the Company’s exposure to subprime loans reported in this filing, Fannie Mae again did not include at least $43 billion of EA loans, included loans from only fifteen loan originators of the approximately 210 lenders listed on the HUD Subprime Lender list, and did not even have the capacity to track whether loans were originated by a subprime division of a large lender”(SEC Complaint, ¶7).

SEC Complaint v. Fannie Mae Executives, 11 CIV 9202, filed Dec. 16, 2011

Until March 20, 2007, New Century was one of the “Fannie Fifteen” loan originators. “By February 2007, following S&P’s downgrade of high-profile subprime lender, New Century Financial Corporation, and other indicia of subprime market turmoil-including HSBC Holdings PLC’s announcement that the U.S. subprime market was unstable-investors were increasingly focused on subprime loans and the risks associated with these loans” (See SEC Complaint, ¶81).

Ethics panel examines lawmakers’ Countrywide loans

By June 2008, Countrywide Financial Corp. was feeling the heat and cooking with Congressional lawmakers.

A Congressional ethics panel began examining allegations that two Senate Democrats, including the sponsor of a major housing bill, received preferential loans by troubled mortgage lender Countrywide Financial Corp. “Friends of Al” refinances popped up all over Washington, DC and throughout state legislatures, when average American Homeowners couldn’t even get a modification. Friends of Al also surfaced in the halls of the Hawaii Legislature. Mazie Hirono even provided a special Countrywide phone number to her constituents that called with foreclosure problems.

“Sen. Christopher Dodd of Connecticut and Sen. Kent Conrad of North Dakota have acknowledged that they refinanced properties as members of Countrywide’s VIP program.”

So, here we are with two major wholesale lenders (among others) under federal investigation, one of which, Countrywide, was schmoozing Congressional representatives. In addition, complicit GSEs were helping them to “Hustle” homeowners with relaxed underwriting guidelines …and along comes Barry and Tim.

As the mortgage world begins to collapse, credit freezes and Lehman Brothers fails, Barack Obama and Tim Geithner begin to “Foam the Runway” for the banks by creating the fake HAMP program that is carried on TV, radio & newsprint inducing homeowners to call to get a modification.

Neil Barofsky, who gave up his job in 2008 as a prosecutor in the U.S. Attorney’s Office in New York City where he had convicted drug kingpins, Wall Street executives, and perpetrators of mortgage fraud, to become the special inspector general in charge of oversight of the spending of the TARP bailout money explains it in detail in his book BAILOUT.

TARP – the program American homeowners thought Congress and former President Obama had constructed for their rescue. Wrong.

Mr. Barofsky writes early on that “I had no idea that the U.S. government had been captured by the banks,” and at another point describes his strategy to use the press to get the attention of Congress, and by extension an obstreperous Treasury: “Our message was simple: Treasury’s desperate attempt to bail out Wall Street was setting the country up for potentially catastrophic losses.””

Mr. Barofsky continues, “One particularly pernicious type of abuse was that servicers would direct borrowers who were current on their mortgages to start skipping payments, telling them that they would allow them to qualify for a HAMP modification. The servicers thereby racked up more late fees, and meanwhile many of the borrowers might have been entitled to participate in HAMP even if they had never missed a payment. Those led to some of the most heartbreaking cases. Homeowners who might have been able to ride out the crisis instead ended up in long trial modifications, after which the servicers would deny them a permanent modification and then send them an enormous “deficiency” bill.”

We knew there was an intended systemic abuse with the modification programs.

Too many people told the same stories. However, we didn’t know why the government, our President and Congress, would allow such abuses but after you read Chapter 8 – it becomes quite clear. Geithner and Obama were saving the banks – not America.

“Making matters worse,” Mr. Barofsky writes, “Treasury all but paved the way for outright fraud by ignoring my recommendations that it kick off HAMP with a broad nationwide television and radio advertising campaign that would educate homeowners about program details and warn them of the dangers of program-related fraud. [. . .] They failed to do so, and, as I had predicted, the chaos of HAMP lured a host of criminal predators running fraudulent advertisements for “guaranteed Obama modifications” from coast to coast.” … including Hawaii and Alaska.

Meanwhile, back at the GSE ranch – Fannie, Freddie and the banks (and a litany of questionable attorneys and document companies) were crafting Assignments of Mortgages by the 10s of thousands – more likely millions. Robo-signers galore forged documents in the millions.

One case where the homeowner is still fighting for his home and currently (at this very moment) facing eviction was another New Century Mortgage origination from January 2007, that had 5 different mortgage assignments (sales/transfers), 5 different banks and 6 different servicers in a short period of time. A major paper shuffle that has confused all parties including the courts. In fact, the last assignment occurred during the foreclosure process and the assignee was never named in the foreclosure complaint. At no time did any of the 6 servicers advise the homeowner that they worked for Fannie. That wasn’t discovered until research into to the servicers’ 10Ks identified FMNA as their primary account.

This case is extremely gruesome because the property has been in the homeowner’s family for 100 years. The case and its manipulation is much too complicated for average attorneys and lower court judges with no securities experience. The five assignments of mortgage apparently confused all including opposing counsel, the foreclosure commissioner, the homeowner’s counsel, and the courts.

The foreclosure complaint was filed on August 19, 2014 and included 4 of the 5 Assignments of Mortgage. Here are some of the highlights of this case:

The first assignment of mortgage is the breeder document from which all the following assignments are derived, was manufactured by or for America’s Servicing Company (ASC) aka Wells Fargo and dated November 4, 2009 and notarized on November 4, 2009. The document assigned the mortgage to HSBC Bank USA. It was signed by well-known robo-signer Lorrie Womack as Asst. Sec. for Mortgage Electronic Registration Systems, Inc.(MERS) as Nominee for New Century Mortgage Corporation. Below – the document on the right belongs to this homeowner. The document on the left is a clone and was filed at the same time – one number off to someone else on another island.

This deceptive breeder assignment fails for several reasons, primarily because New Century was in a liquidating bankruptcy and as of April 25, 2008, by order of the bankruptcy court, was no longer associated with MERS. The homeowner presented all of the documented evidence, but the lower Hawaii circuit court ignored the entire argument – it appears, so did the attorney that took over his case. Hawaii courts routinely ignored robo-signing and forgery in foreclosure cases. Bankruptcy court orders also carried no weight – even if the there was no legal authorization for the creation of the assignment.

On February 5, 2016, the Board of Governors of the Federal Reserve System (FRS) issued an Order of Assessment of a Civil Money Penalty Issued Upon Consent Pursuant to the Federal Deposit Insurance Act, as Amended (“FRS Order”) against HSBC North America Holdings, Inc. NY, for its deceptive and failed business practices with regard to mortgage loans from January 1, 2009 to December 31, 2010. Stating, pgs. 2-3, in part:

“Filed or caused to be filed in state courts [. . .] or in the local land record offices, numerous affidavits and other mortgage-related documents that were not properly notarized, including those not signed or affirmed in the presence of a notary;

HSBC NY case no. 12-011-CMP-HC

Litigated foreclosure [. . .] without always confirming that documentation of ownership was in order at the appropriate time, including confirming that the promissory note and mortgage document were properly endorsed or assigned and, if necessary, in the possession of the appropriate party;

HSBC settled with FHFA (GSE Conservatorship) for $550 million. The suit on behalf of Fannie and Freddie accused bank of misrepresenting toxic subprime MBS that helped send the pair into conservatorship. The HSBC corruption matching the breeder assignment of mortgage document apparently didn’t phase the court either. The judge conveniently over-looked the corruption documentation.

At one point during this fiasco, both Wells Fargo and HSBC were trying to collect on this loan at the same time, sending the homeowner confusing letters shortly after he had been advised to skip 3 payments in order to qualify for HAMP. Throughout the process the homeowner, a former police officer, tried numerous times to get a HAMP modification through ASC to no avail.

If ever there was a poster child for foreclosure and mortgage securitization corruption – this is it! (and these are only the highlights)

The plaintiff in this foreclosure case is US BANK TRUST, NATIONAL ASSOCIATION AS TRUSTEE FOR WG2 MORTGAGE TRUST VII, SERIES 2013-1 (the 4th assignment of mortgage from WG1 Mortgage Trust VII through Morgan Stanley Mortgage Capital Holdings LLC) and Saxon Mortgage Services to WG2.

In late 2010, another servicer, Saxon Mortgage Services, Inc. (Saxon) took over the loan indicating a new loan number. Every servicer changed the loan number without notice, of course making it even harder to track even by professionals. Saxon also entered into a Commitment to Purchase Financial Instrument and Servicer Participation Agreement with the U.S. Treasury and FANNIE on September 24, 2010 which was terminated for cause by Fannie on April 9, 2013. The timing of Saxon servicing issues correlates with the Federal Reserve Board announcement on April 2, 2012 issuing a Consent Order against Morgan Stanley to address a pattern of misconduct and negligence in residential mortgage loan servicing and foreclosure processing at its subsidiary, Saxon.

Then followed Specialized Loan Servicing (“SLS”), who also entered into a Commitment to Purchase Financial Instrument and Servicer Participation Agreement with the U.S. Treasury and FANNIE on January 13, 2010 replacing the previous servicer.

All of the homeowner’s loan servicers entered into these Fannie Servicer Participation Agreements to modify loans which were in full force and effect as they serviced the loan.

https://www.treasury.gov/initiatives/financial-stability/TARP-Programs/housing/mha/Pages/contracts.aspx

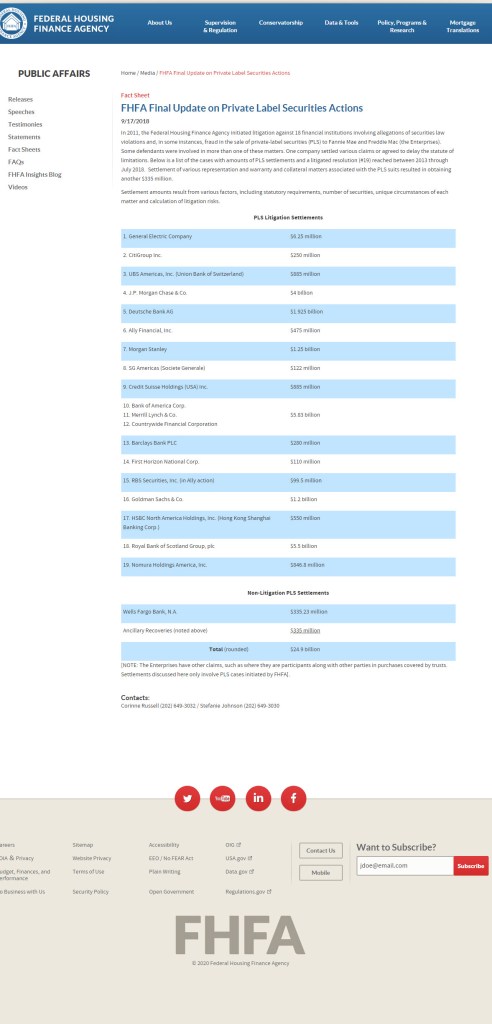

By December 30, 2013, Wells Fargo & Co agreed to pay $335.23 million to Fannie to settle claims of fraud and deception over defective home loans – IN PRIVATE LABEL SECURITIES (PLS). In February 2014, Morgan Stanley agreed to pay FHFA $1.25 Billion to settle a lawsuit that it sold mortgage bonds to Fannie and Freddie without adequately disclosing their risks.

On November 19, 2013, enters another servicer, LenderLive Network Inc. (“LenderLive”), that took over the loan servicing until October 26, 2014. LenderLive was an “Approved Fannie Seller/Servicer.” On December 18, 2013, LenderLive sent the homeowner a letter stating, “LenderLive Network is servicing your account on behalf of WG2 Mortgage Trust VII.” The Assignment of Mortgage from WG1 to WG2 was signed and notarized on March 18, 2014.

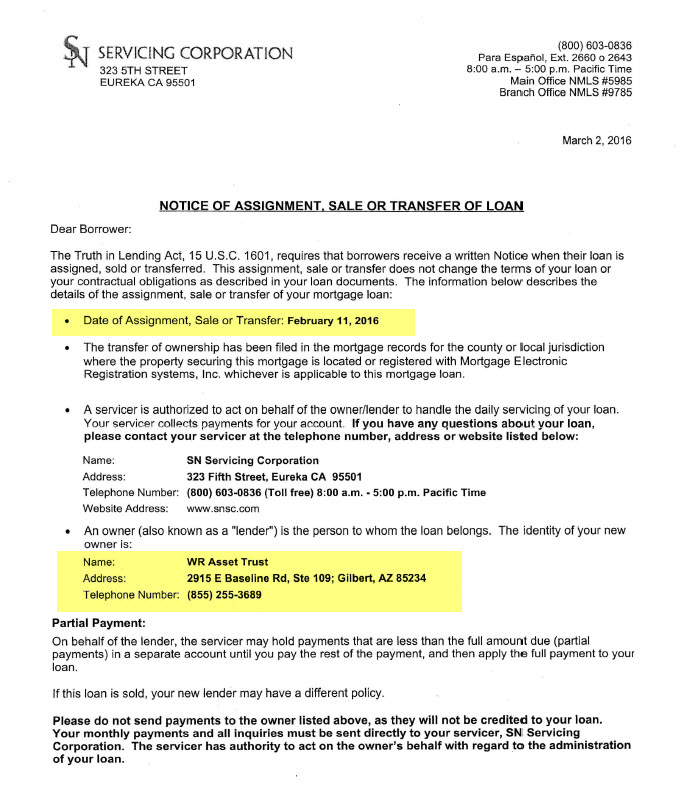

Once again another servicer, SN Servicing, sends a 5th Notice of Assignment, Sale or Transfer of Loan letter to the homeowner dated March 2, 2016 that there is yet another “owner (aka “lender”) is the person to whom the loan belongs. WR Asset Trust (“WRAT”) claimed the loan on February 11, 2016. WRAT is never brought forth into the foreclosure case or even addressed. The documentation before the court was again ignored.

WRAT is actually WR Asset Trust aka Window Rock Residential Recovery Fund, L.P., Window Rock Capital Partner GP, LLC, Window Rock Manager, LLC, WINDOW ROCK INVESTMENT OPERATIONS, LLC, all located at 2915 E Baseline Rd, Ste 109, Gilbert, AZ 85234-2427.

During this entire period the homeowner was trying to obtain information and a decent modification of his loan. His loan (along with millions of others) was a hot potato, caught up in a whirlwind of deceit and toxic mortgage allegations. The servicers were not following through. The servicer and loan statements changed hands so many times it was hard to keep up with who owned the servicing rights let alone the loan, who to talk to, how much was owed, and where to send payments.

Plaintiff’s Verified Complaint filed August 19, 2014 was preceded by actions taken against all of the banks, related to homeowner’s loan history, for crimes and deception carried on before and during:

The 2011 Office of the Comptroller of the Currency (“OCC”) Consent Orders;

The 2011 SEC Complaints & Settlements

The 2011 FHFA, as conservator of Fannie and Freddie Complaints & Settlements;

The 2011 FHFA Complaints & Settlements;

Federal Reserve Consent Orders:

U.S. Commodity Futures Trading Commission Orders;

The 2012 DOJ v. Banks Complaints & Settlements;

The 2012 National Mortgage Complaint & Settlement.

These investigation cases, orders and ‘settlements with admissions’ that followed made clear the wrong doings, fraud, and, falsified documents, such as the breeder assignment, were evidence of a scheme. Documents should have been extracted from public files as ordered and properly corrected – but they weren’t. In Hawaii, none of the orders were adhered to, ordered, or even considered by the foreclosure courts.

It’s now September 2020. The homeowner has been hammered. He and his son are about to be evicted, his attorney was just disbarred. He starts looking over his file and realizes that something is askew. On July 12, 2020, opposing counsel filed a declaration including a the foreclosure commissioner’s report where the property was sold to the 4th Assignment of Mortgage assignee/Plaintiff without even a mention of WRAT – the 5th assignee. No documents were produced have relinquished the WRAT Assignment of Mortgage, even if it were valid. And there was nothing filed in his defense.

These are just 2 incidences above, of probably millions that have been so heavily manipulated over the last 12 years that FHA loan identifiers are just buried. We know the Treasury, Fannie (as financial agent for the United States, and the Federal Reserve hold the majority of these loans that were once in the fraudulent REMIC trusts. The Foreclosure & Eviction Moratorium should apply to all loans stemming from Mortgage Electronic Registration Systems, Inc. (a 1999 Fannie & Freddie created entity), as well as banks that participated in the securitization scheme through 2009.

We humbly ask that you, President Trump and Secretary Ben Carson, make the Foreclosure & Eviction Order inclusive enough to fight the manipulation of the securitization/rehypothecation mortgage documents abuse – no matter from where it stems – because American Homeowners understand how manipulated and corrupt the mortgage system was and continues to be. And we all need American Homeownership to remain healthy as it is a primary staple representing the greatness and freedom in our Republic.

Good job just hoped you could have given both of our names in a private message to our president to see if he would send investigators to investigate and oversee the way the justice in our courts have been unjust and unfairly detrimental to homeowners.

Sent from my iPhone

>

I seriously doubt that POTUS Trump or Ben Carson will read it.

Thank you for standing up for homeowners. I still have no idea what will happen with our mortgage as we were put into a loan that had been banned by our state in 2002 but we were put into it in 2006 after a 2004 Fannie Mae debacle by Countrywide and Left in them by Bank of America and Specialized Loan Services. We are now going on 7 years with not paying the mortgage and being left in this predatory option arm that was negatively amortizing. They have never attempted foreclosure and now are sending us delinquency letters. The SLS and SEC have our loan being owned by CWALT or Countrywide Alternative Loan Trust. I would think that if Countrywide is bust, that CWALT is bust. But cannot get a straight answer anywhere. So thank you for this article that gives me more when and if they finally try to foreclose.

Thank you for sharing this valuable information in this letter.I am still fighting with Freddie Mac & FHFA(co-conspirators) who joined the deception with the banks ,tried to evict me from my home.Iâve been appreciative! Sent from Mail for Windows 10 From: Deadly ClearSent: Saturday, September 19, 2020 12:40 AMTo: creatreyk@gmail.comSubject: [New post] An Open Letter to President Donald J. Trump & HUD Secretary Ben Carson Deadly Clear posted: " Regarding the 2020 Foreclosure & Eviction Moratorium By Sydney Sullivan For nearly a dozen years, we have followed the securitization/rehypothecation crisis and corruption on behalf of over 200 million American Homeowners (2.5 per HH) and their"

I have not found any court record so far in my case nor my sons where the party the lawyers purport to represent have given a testimony witnessing a cause of action. Only the servicers and lawyers whom we all know are frauds. See the law of Voids

Only DBNTC and the Erickson’s can testify on behalf of our cases: DBNTC has never testified in any of the cases pro se in Judge Pechmans court, nor in Judge Darvas court in Superior court in Kent WA. Nor in Judge Benders court of record.

SEE LAW OF VOIDS; Before a court (judge) can proceed judicially, jurisdiction must be complete consisting of two opposing parties (not their attorneys – although attorneys can enter an appearance on behalf of a party, only the parties can testify and until the plaintiff testifies the court has no basis upon which to rule judicially), and the two halves of subject matter jurisdiction = the statutory or common law authority the action is brought under (the theory of indemnity) and the testimony of a competent fact witness regarding the injury (the cause of action). If there is a jurisdictional failing appearing on the face of the record, the matter is void, subject to vacation with damages, and can never be time barred.

“Lack of jurisdiction cannot be corrected by an order nunc pro tunc. The only proper office of a nunc pro tunc order is to correct a mistake in the records; it cannot be used to rewrite history.” E.g., Transamerica Ins. Co. v. South, 975 F.2d 321, 325-26 (7th Cir. 1992); United States v. Daniels, 902 F.2d 1238, 1240 (7th Cir. 1990); King v. Ionization Int’l, Inc., 825 F.2d 1180, 1188 (7th Cir. 1987). And Central Laborer’s Pension and Annuity Funds v. Griffee, 198 F.3d 642, 644(7th cir. 1999).

1. . There has not been any record file with the court of a competent fact witness, or even a claim of damages by an official of DBNTC as Trustee for LBML 2006-4, which is contract law the trust is the contract, that governs this court and has never been put on court record before the court .. 2. There is no record with this court of the Trust Contract defendants purport to represent, it is missing in action 3. There is no claim of damages by a DBNTC employe only a hearsay employ of the servicer and the lawyers.

Virginia does a great job of putting these wonderful articles together.

In 2012 The Five largest Financial Institution in this nation entered into a Consent Judgment against them for criminal violations of Mortgage lending Law in this nation. This was NOT a settlement NOR was it an agreement. This judgment was a consent plea that the DOJ, Federal Regulators, US Attorney General and State Attorney Generals accepted. These Financial Institutions consented to Judgment to avoid criminal prosecution of their Executives. All State and Federal Mortgage Lending Laws are written to protect the “Borrowers/Private Land owners?Homeowners” of this nation. The penalty for violations of these Laws is in criminal in nature and depending on whether the violation was a once time offense or multiple offenses, depending on whether the violation constituted a felony or habitual crimes, the penalties range from fines to time in prison for each and every offense. Our American Justice System should not be allowing these consenting offenders inside the courtroom doors to try to attempt to continue to profit from their crimes.

HOMEOWNERS LEGAL RIGHTS INC.

Linda Nash CEO

Absolutely correct!