Dual tracking is when a servicer has you filling out modification paperwork and sending them your bank statements, proof of residency, tax returns, P&Ls, payroll stubs, etc. (over and over) and actually is processing your foreclosure at the same time. Homeowners were supposed to be protected from dual tracking during modification.

Dual tracking is when a servicer has you filling out modification paperwork and sending them your bank statements, proof of residency, tax returns, P&Ls, payroll stubs, etc. (over and over) and actually is processing your foreclosure at the same time. Homeowners were supposed to be protected from dual tracking during modification.

But in case you were wondering if you can sleep at night while under the modification game – here are some interesting facts just released from the California Reinvestment Coalition (CRC) who distributed a survey to housing counselors in February 2013 to Report on how the banks were holding up their end of the bargain. So, if California is any indication of what the banks are doing around the rest of the country – be very wary.

The Report cites:

“Dual track violations persist

For years, housing counselors and advocates have decried the harm caused by dual track practices. These abuses were addressed in both the Attorney Generals’ National Mortgage Settlement (NMS) and the Homeowner Bill of Rights (HBOR), giving cause for optimism that borrowers might finally receive fair consideration for a loan modification before foreclosure. Counselors do report fewer dual track violations but violations continue with all servicers, and some counselors report concerns that servicers are using loopholes to evade dual track protections.

For years, housing counselors and advocates have decried the harm caused by dual track practices. These abuses were addressed in both the Attorney Generals’ National Mortgage Settlement (NMS) and the Homeowner Bill of Rights (HBOR), giving cause for optimism that borrowers might finally receive fair consideration for a loan modification before foreclosure. Counselors do report fewer dual track violations but violations continue with all servicers, and some counselors report concerns that servicers are using loopholes to evade dual track protections.

![]()

Dual Track Violations

- Over 60% of counselors reported that Bank of America, Citibank, JPMorgan Chase and Wells Fargo still dual track “sometimes,” “often,” or “always,” even though this abusive practice should have ended months ago, under the NMS.

- Ally was the only servicer that was reported by a majority of responding counselors to only “rarely” or “never” dual track.

- When asked about the performance of “all servicers,” counselors were even more likely to note violations. 72% of counselors responding reported all servicers “sometimes,” “often” or “always” dual track, and only 8% of counselors said that they never see dual track violations. This is incredibly concerning since dual track was supposed to have ended among the Big 5 with NMS, and with all servicers under HBOR.

When asked, “which servicers are the biggest dual track offenders?” counselors listed:

When asked, “which servicers are the biggest dual track offenders?” counselors listed:

- Bank of America – 19 times

- Wells Fargo – 18 times

- JPMorgan Chase – 9 times

Emerging Issue: “Complete Loan Modification Application”: Dual track and other protections kick in for borrowers when they are deemed to have submitted a complete loan modification application. But what does this mean, and how is this communicated to a borrower?

- Large percentages of responding counselors noted that homeowners are not told if and when a loan modification application is complete, even after submitting all documents requested.

- Bank of America fared worst, with nearly half of responding counselors saying this was “always” or “almost always” the case.

- Ally performed “best,” with less than 20% of counselors saying Ally “always” or “almost always” fails to tell homeowners when their loan modification applications are complete.

![]()

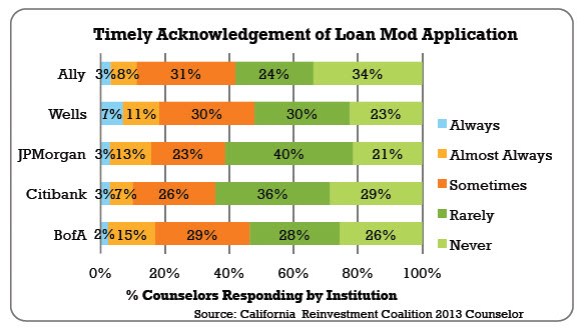

Servicers are flouting the timelines established by the NMS

The NMS required the largest servicers to follow specific uniform timelines for loan modification requests. Borrowers are supposed to receive a written acknowledgement of their loan modification applications within 3 business days, notification of any missing documentation in 5 days, 30 days to respond to a request for additional documentation, and 30 days to receive a final decision upon their loan modification application being complete. Most of the counselors responding noted that these timelines are “rarely” or “never” being met by all institutions, for nearly all timeline obligations.

- A majority of counselors said each of the Big 5 Banks “rarely” or “never” acknowledged receipt of a loan modification application within 3 business days. For Citibank, over 60% of respondents noted this poor performance.

- A majority of counselors said each of the Big 5 Banks “rarely” or “never” notified homeowners of documents needed to complete their loan modification applications within 5 business days. For JPMorgan Chase, over 60% of respondents noted this poor performance.

- Over one-third of counselors said each of the Big 5 Banks “rarely” or “never” gave borrowers 30 days to respond to a request for additional documentation. For Citibank and Ally, over half of counselors noted this poor performance.

- Sixty percent or more of counselors said each of the Big 5 Banks “rarely” or “never” made loan modification decisions within 30 days of a complete loan modification application having been submitted. For Bank of America and Citibank, over three-quarters (75%) of counselors noted this poor performance.

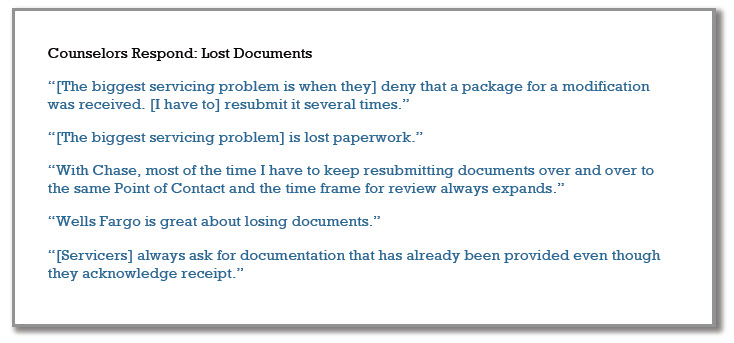

Lost Documents. It is hard to imagine that servicers have not fixed this problem, but counselors continue to report that servicers lose documents, as well as take too long to act on loan modification applications and then need to request the same documents over and over again.

- Over 60% of counselors reported that Bank of America, Citibank, JPMorgan Chase, and Wells Fargo lose documents at least “sometimes.” Ally fared better with “only” 49% saying Ally loses documents at least “sometimes”.

- Over a third of responding counselors said Bank of America lost documents “always” or “almost always.”

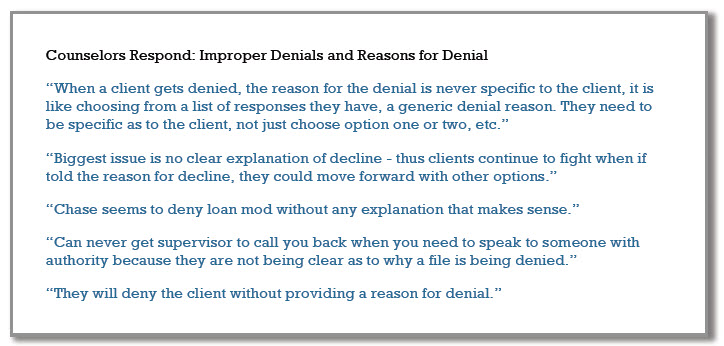

Housing counselors believe that borrowers are being turned away when they do qualify for help that would save their homes. Counselors also report that when denials are made, banks fail to provide the reasons for denial, as required by the NMS and HBOR.

- Over 60% of responding counselors felt that each of the Big 5 servicers denied loan modifications to seemingly qualified homeowners, at least “sometimes.”

- Wells Fargo performed worst, with over a third of all responding counselors saying Wells denied seemingly qualified borrowers “always” or “almost always.”

- When questionable denials were given, the reasons for denial were often unclear. Well over half of all responding counselors felt that each of the five banks denied loan modifications without offering an understandable explanation for the denial, at least “sometimes.”

- Bank of America, JPMorgan Chase and Wells Fargo were cited by over 30% of responding counselors as “always” or “almost always” failing to provide understandable reasons for loan modification denials.”

Maybe because they all wrote more loans than they can legally hold…”Ah, CRC please don’t tell the bank regulators but if we kept all the good loans we’d be out of business…”

http://stopforeclosurefraud.com/2013/04/09/foreclosure-settlement-a-nationwide-crime-scene-all-in-w-chris-hayes/ Our entire nation is a crime scene including our courts.

Yep! Yes! and yes to all of the above in my 2 year losing battle with B of A… Absolutely criminal.

Sorry to hear they won Gene…I am the queen of dual track… All of the above also applied to me as well with BofA. They finally modified but only because I paid someone a large amount of cash to get down in the dirt and fight with me tooth and nail and she had connections with their social media team. They decided they wanted to modify and so everything went through smoothly, no more lost docs and other shell game tactics. But at the time of modification my happiness was beset by the realization that they had added massive compounded arrearage, interest and whatnot to the end of my loan. They billed me for the year and a half of dual tracking, the failed original approved HAMP that never should have been so delayed (not crediting those payments correctly) their CONSTANT stalling and denials and their foreclosure mill attorney fees for a foreclosure proceeding that never should have happened in the first place. In the end they ripped me off for at least $30K more than they deserved to get. Oh, and my house is still waaay underwater.

Kristina, I am currently going thru this. I missed 5 payments due to job loss and filled out all the paperwork directly to Fannie Mae and the loan servicer, Ocwen. I did all the paperwork-bank statements, pay stubs, hardship letter, etc. They said I was approved for trial modification which I completed and then entered into the modification. While they sent me the approved modification letter and I started sending the new payment they said it was not actually approved because there was a problem with the title(a complete lie). I had to send non identify affidavits etc. They lost the documents several times and then said they were transferring the loan servicing to Seterus. Now Seterus said they are offering me another trial modification and at the same time sent me a certified letter saying I am in default with “intent to foreclose”, because Ocwen never applied ALL of those payments I sent in to the trial modification and regular modification. I am definitely getting the run around and feel completely screwed. Can you give me the name of the person who helped you? I have three kids and feeling desperate, heart broken and completely taken advantage of. Sorry to give you my long sob story. Any help appreciated

Don’t let these Banks scam anybody else by foreclosing on them. I started my modification process with Wells Fargo Dec 19th, 2012. My package was completed on Apr 2, 2013. After multiple phone calls to my home preversation, foreclosure dept i never received a call back. Time was running out and i expressed this several times.

Desperate, I replied to a brochure(advertising 12 diff foreclosure programs) from Mission Bishop Century 21 realtors. They thought they convinced me I had no options left but to sell my house once a found the sale date posted on my door. NOPE think again the broke the law of Duel Tracking,

I’ve contacted an attorney who is going to get the sale stopped and modify me. Spread the word on duel tracking people are losing their houses left and right because they don”t know about this, If you need a repetable attorney contact me,

Attorney Please.

Pingback: Mortgages that do not qualify for a loan modification | Loan Modification Explained