The authors of In Defense of “Free Houses” – Yale Law students Megan Wachspress, Jessie Agatstein and Christian Mott have taken a surface view of an extremely deep and dark lake of fraud, criminal behavior and intent.

The authors of In Defense of “Free Houses” – Yale Law students Megan Wachspress, Jessie Agatstein and Christian Mott have taken a surface view of an extremely deep and dark lake of fraud, criminal behavior and intent.

Understanding the depth of the mortgage securities related corruption would need several scuba dives to get behind the 1990’s intentionally orchestrated criminal behavior. Researchers like Ken Dost and a host of others, discovered some of the keys to the intent of the overall process hidden in plain site in the USPTO where the banksters patented nearly every move beginning prior to inception of the transaction all the way to death of a mortgage – all “seamlessly automated.”

Whether you believe in right to life and/or freedom of choice, homeowner mortgages and collateral never had a chance. The abortion started before the first signature was ever penned on the faux mortgage and note. Free Houses authors write:

“Banks have lost many foreclosure cases for two reasons, both resulting from recent changes in the mortgage market. First, securitization has created widespread errors in mortgage notes’ chains of assignment, making it difficult for banks to prove that they in fact own any particular mortgage. Second, securitization contracts incentivize banks to use “foreclosure mill” law firms to keep up with the flood of defaults, despite the fact that these firms are unable and sometimes unwilling to detect and rectify basic legal errors.”

This statement is weak because if they consider 20+ years of calculated changes to be “recent” – then it appears the young authors are missing the point that this chaos was well-orchestrated and intentional. It did not just happen yesterday, last week or last year.

In order to make this NEW – non-traditional mortgage securitization work the way it was intended – you must consider the changes to the UCC and the creation of Mortgage Electronic Registration Systems, Inc. back in 1992/1993, and look at deregulation of the 1990s.

“President Clinton’s tenure  was characterized by economic prosperity and financial deregulation, which in many ways set the stage for the excesses of recent years. Among his biggest strokes of free-wheeling capitalism was the which repealed the Glass-Steagall Act, a cornerstone of Depression-era regulation. He also signed the Commodity Futures Modernization Act, which exempted credit-default swaps from regulation. In 1995 Clinton loosened housing rules by rewriting the Community Reinvestment Act, which put added pressure on banks to lend in low-income neighborhoods.” (See TIME)

was characterized by economic prosperity and financial deregulation, which in many ways set the stage for the excesses of recent years. Among his biggest strokes of free-wheeling capitalism was the which repealed the Glass-Steagall Act, a cornerstone of Depression-era regulation. He also signed the Commodity Futures Modernization Act, which exempted credit-default swaps from regulation. In 1995 Clinton loosened housing rules by rewriting the Community Reinvestment Act, which put added pressure on banks to lend in low-income neighborhoods.” (See TIME)

Banks intentionally lobbied for these changes because they had a specific purpose in mind and the old laws stood in the way of the banks using property as their new gold standard. Look at the damage that was done under the Clinton administration.

Securitization did not create the “errors in the mortgage notes.” That too was intentional. The loan documents, most of which as Mr. Dost has noted, are copyrighted forms licensed for use by Fannie Mae and Freddie Mac through a third party.

The traditional looking note, for example, as homeowner Daneford Wright has pointed out to his attorney, was intended to appear and be considered the “original” document, just as it was 15-20+ years ago. The homeowner note, in most cases, refers specifically to “this note” 28 times in the contract document.

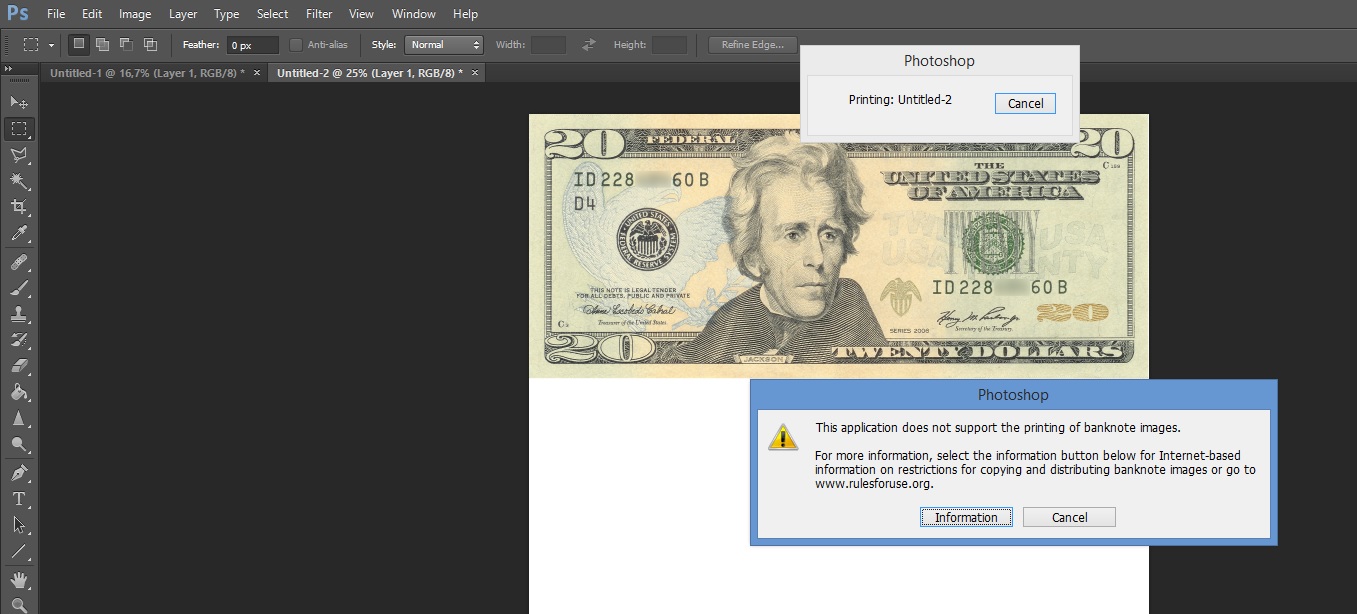

As a homeowner, you  expect to be getting “this (same) note” back when you have paid off your debt, not a Xerox copy of it downloaded from a computer program to which hundreds, if not thousands of people have access. Think about it, wouldn’t it be great if you could make a copy of a check and try to cash it – or copy a store receipt and return an item – how about copies of a $50 bill?

expect to be getting “this (same) note” back when you have paid off your debt, not a Xerox copy of it downloaded from a computer program to which hundreds, if not thousands of people have access. Think about it, wouldn’t it be great if you could make a copy of a check and try to cash it – or copy a store receipt and return an item – how about copies of a $50 bill?

Isn’t it considered counterfeiting when you print copies of real money and try to pass them off as a real negotiable instrument?

The mortgage also refers to the specific (“this”) note. The faux documents were intentionally made to appear traditional – when in fact they were nothing more than facades to get homeowners to think they were executing traditional documents for a traditional transaction – when it appears the procurement of their collateral had already been sold (nemo dat) before they signed.

The notes, the ARMS, the new financial products were all set up on purpose to increase defaults. Fraud safeguards were built into the banksters’ software but intentionally relaxed to access more victims. Defaults are necessary in order to maintain bank liquidity. And liquidity was promised to the investors – pension fund investors must have liquid and Triple A vehicles in order to invest. Foreclosures and resales will bring liquidity – if no one fights it and the judges side with the banks.

Of course foreclosure judges and legislators want to side with the banks because some (if not most) of their pension funds and investments are also on the line. It took some doing – and planning (and certainly not a “recent” task) to get the state and federal governments and the unions to agree to invest in these new Wall Street securities – especially after RTC v. Key Financial. But the investment banks were quite successful – there is hardly a state or federal pension fund anywhere that doesn’t own mutual fund investments that have a sizable amount of worthless mortgage-backed securities and/or other derivatives – making it difficult not to consider their own future when it comes to making a decision in favor of a bank – and that too, it appears, was part of the overall plan.

Of course foreclosure judges and legislators want to side with the banks because some (if not most) of their pension funds and investments are also on the line. It took some doing – and planning (and certainly not a “recent” task) to get the state and federal governments and the unions to agree to invest in these new Wall Street securities – especially after RTC v. Key Financial. But the investment banks were quite successful – there is hardly a state or federal pension fund anywhere that doesn’t own mutual fund investments that have a sizable amount of worthless mortgage-backed securities and/or other derivatives – making it difficult not to consider their own future when it comes to making a decision in favor of a bank – and that too, it appears, was part of the overall plan.

“Second, securitization contracts incentivize banks to use “foreclosure mill” law firms…” Rather, it’s the patented software programs – the “seamlessly automated” programs from the Fannie Mae 1003 loan application software all the way through default and assignments, etc. and foreclosure to REO. The process is completely patented and as Mr. Dost has stated numerous times – it was intentionally designed to operate in a certain way. The algorithms are paramount in this process. It’s not the contracts that incentivize the banks.

There are good points in the paper – it just misses the mark that, however screwed up the securitization system may appear – the overall process began a long time ago and was intentionally constructed.

There are good points in the paper – it just misses the mark that, however screwed up the securitization system may appear – the overall process began a long time ago and was intentionally constructed.

Without confiscating a complete mortgage sale and mortgage servicing computer system and/or delving into the USPTO software patents and trademarks it would be very difficult to put the pieces together. As Judge Peck of the bankruptcy court in the Southern District of New York observed, mortgage-backed securities are “unique creatures of Wall Street . . . and it is the rare ordinary human being who understands them.”

The authors are correct that “free houses” should be defended – but calling them “free” is a real misnomer. Homeowners were suckered into tricky dicky investments though contracts where the real intent was concealed… no disclosure… and the instruments that were used just for show and inducement – and, of course, it appears intended to be relied upon. Homeowners’ collateral was gambled and compromised by Wall Street without their consent or knowledge. If the intent and reliance factors were to be recognized – real judges would throw the fabricated and photo copied documents our of their court and hold tight to the contact terminology and demand that “this note” – the original note, not a copy thereof – be supplied, or else dismiss the claims with prejudice.

The moral hazard lies with the banksters’ and their cohorts’ deception and intent to deceive, the failure to disclose, the intentionally inflated appraisals and the sick and intentional manipulation of the American homeowners’ reliance for the one and only purpose of demented capitalistic profit. When you make a photo copy of a negotiable instrument or cash and try to pass it off as an original – there is intent to deceive.

The moral hazard lies with the banksters’ and their cohorts’ deception and intent to deceive, the failure to disclose, the intentionally inflated appraisals and the sick and intentional manipulation of the American homeowners’ reliance for the one and only purpose of demented capitalistic profit. When you make a photo copy of a negotiable instrument or cash and try to pass it off as an original – there is intent to deceive.

The saddest outcome of all of this is that the judges and the governments think they are holding the country together, when in fact, by allowing this type of man-made computerized criminal behavior they are merely adding to the country’s overall moral degradation and physical decay. And for what? For pensions, retirement funds and investments that, more than likely, are not there anymore anyway? Wake up!

And with that, as Naked Capitalism posted: “I encourage you to read the article in full:”

I have been defending myself with the help for http://www.jtadvocates.com for years against Wells Fargo, my admitted debt collector. Not my lender. Initially, the principle on my mortgage was paid ahead due to years of me paying my mortgage biweekly. They, Wells Fargo”s home preservation specialist, Christine, told me I had to be 90 days delinquent on my mortgage to even apply for a modification. I called back months later and was allowed to apply for a modification. They dual tracked me, charged me illegal monthly fees, provided me with the names of 4 different lenders when asked and was unable to produce the original note. The court process was laughable, as Judge Suter, Mt Holly civil court upheld no laws and allowed the banisters to have their way with me and the courts. She overlooked documents, laws and even the cannons that govern her. It was an unreal experience. When asked to recuse herself she refused. Needless to say I ended up homeless.

What a great brief done by 3 yale students regarding the banks and foreclosures. A great copy and paste for Paul.