In 2010, Meg Rehrauer, a J.D. Candidate at Northeastern University School of Law, wrote a memorable paper:

REGAINING THE WONDERFUL LIFE OF HOMEOWNERSHIP POST-FORECLOSURE DEFENDING HOMEOWNERS FROM EVICTION AFTER FORECLOSURE BY ATTACKING THE OWNERSHIP RIGHTS OF THE FORECLOSING ENTITY

REGAINING THE WONDERFUL LIFE OF HOMEOWNERSHIP POST-FORECLOSURE DEFENDING HOMEOWNERS FROM EVICTION AFTER FORECLOSURE BY ATTACKING THE OWNERSHIP RIGHTS OF THE FORECLOSING ENTITY

It’s Christmas 2 years later and we’re still reeling in foreclosures and frauds committed by the banks because America is stuck in the portion of George Bailey’s dream as if he hadn’t been born.

“But he did help a few people get out of your slums, Mr. Potter. And what’s wrong with that? Why… Here, you’re all businessmen here. Doesn’t it make them better citizens? Doesn’t it make them better customers? You… you said… What’d you say just a minute ago?… They had to wait and save their money before they even ought to think of a decent home. Wait! Wait for what? Until their children grow up and leave them? Until they’re so old and broken-down that they… Do you know how long it takes a working man to save five thousand dollars? Just remember this, Mr. Potter, that this rabble you’re talking about… they do most of the working and paying and living and dying in this community. Well, is it too much to have them work and pay and live and die in a couple of decent rooms and a bath? Anyway, my father didn’t think so. People were human beings to him, but to you, a warped, frustrated old man, they’re cattle.” Jimmy Stewart as George Bailey, It’s a Wonderful Life (Liberty Films (II) 1946)

Suffice to say anyone in foreclosure considers the Wall Street banks to be Mr. Potter …warped, frustrated old men.

Suffice to say anyone in foreclosure considers the Wall Street banks to be Mr. Potter …warped, frustrated old men.

Ms. Rehrauer begins her paper with the dialogue from the movie above and continues:

“I. Overview

In It’s a Wonderful Life, George Bailey, a local businessman and hero, supported the community by offering townsfolk affordable loans from his Bedford Building and Loan. As Steven M. Cohen, Counselor and Chief of Staff at the Office of the New York State Attorney General, Panel Discussion: The Subprime Mortgage Meltdown and the Global Financial Crisis, Address Before The Eighth Annual Albert A. Destefano Lecture on Corporate, Securities, and Financial Law (Apr. 15, 2008), in 14 Fordham J. Corp. & Fin. L. 1, 20 (2008), explains:

“There’s that great scene where there’s the run on the bank…and the Jimmy Stewart character explains, “Your money isn’t with me. It’s not here behind the counter. It’s in Harvey’s home. That’s where your money is. And Harvey’s money is in Gretchen’s home.” That model

“There’s that great scene where there’s the run on the bank…and the Jimmy Stewart character explains, “Your money isn’t with me. It’s not here behind the counter. It’s in Harvey’s home. That’s where your money is. And Harvey’s money is in Gretchen’s home.” That model

ceased to exist. I don’t know when it ceased to exist, but at some point it did.”

[Ed. note: Steven M. Cohen, was the former federal prosecutor and Chief of Staff for Gov. Cuomo – not to be confused with Steven A. Cohen, Hedge fund trader under possible SEC investigation]

As Mr. Cohen aptly described, the originating lender, or originator, in the modern mortgage business will likely not hold mortgages for the life of the loan. Today, originators commonly sell mortgages, especially at-risk mortgages, to other institutions as part of a securitization process.[3] When securitized, the individual mortgages are pooled together and offered as an investment security.[4] Mortgage companies benefit from recouping their investments and eliminating the risk of non-payment, while investors benefit from the mortgage companies’ reduced transaction costs due to economies of scale and reduced initial capital requirements.[5]”

Although Ms. Rehrauer’s paper is based on the Massachusetts foreclosure process and deals with the unconventional use of Mortgage Electronic Registration Systems, Inc. along with the confusion of the homeowner, it is still relevant in every state:

“When receiving the multiple notices from an unknown lender or MERS, the borrower is often unsure of what she should do next: Who should I negotiate with? What do I do without being able to afford a lawyer? How can I come up with enough money to cure a default? While the borrower contemplates these questions, the lender may foreclose on the property and move to evict the former homeowner. Since Massachusetts is a non-judicial foreclosure state, the borrower will not necessarily have her day in court to defend against the foreclosure. [. . .]

“When receiving the multiple notices from an unknown lender or MERS, the borrower is often unsure of what she should do next: Who should I negotiate with? What do I do without being able to afford a lawyer? How can I come up with enough money to cure a default? While the borrower contemplates these questions, the lender may foreclose on the property and move to evict the former homeowner. Since Massachusetts is a non-judicial foreclosure state, the borrower will not necessarily have her day in court to defend against the foreclosure. [. . .]

When the foreclosure process lags for months, the homeowners may begin to believe that someone or something has intervened, that the lender forgot about the foreclosure, or that the lender has decided to give them a break. Unfortunately, the lender will eventually foreclose on the mortgage and move for eviction. At this point, the homeowners may seek legal counsel, at a time generally considered too late. It is not, however, too late for some homeowners, because a process that is confusing and complicated for borrowers is equally complicated for lenders.

When challenged, some lenders have been unable to show an unblemished ownership interest.[23] Without an unblemished ownership interest in the mortgage prior to foreclosure, the foreclosing entity may not have a clear title to the underlying property.[24] Therefore, when a homeowner faces eviction after foreclosure, it is important to ensure that the foreclosing entity properly owned the mortgage prior to foreclosure. If the entity does not own the mortgage prior to foreclosure, the homeowner may be able to overturn the foreclosure and ultimately remain in her home.

When challenged, some lenders have been unable to show an unblemished ownership interest.[23] Without an unblemished ownership interest in the mortgage prior to foreclosure, the foreclosing entity may not have a clear title to the underlying property.[24] Therefore, when a homeowner faces eviction after foreclosure, it is important to ensure that the foreclosing entity properly owned the mortgage prior to foreclosure. If the entity does not own the mortgage prior to foreclosure, the homeowner may be able to overturn the foreclosure and ultimately remain in her home.

What colloquially is thought of as a mortgage is comprised of two separate legal documents – the note and the mortgage. The note evidences the debt agreed upon determined from the mortgage transaction. This note grants the mortgagee the right to collect payment. The note is a negotiable instrument that is typically not recorded on the registry of deeds.

On the other hand, the mortgage evidences the security interest arising from the mortgage transaction. This mortgage typically grants the mortgagee the right to foreclose and must be recorded with the registry of deeds. Therefore, the right to foreclose arises from the contractual language in the mortgage.[25] Despite the fact that the mortgage grants the right to foreclose, the entity must own both the mortgage and the note in order to do so.[26] Therefore, an assignee must have a valid assignment of mortgage with an indorsement of note in order to assert an ownership interest and have the authority to foreclose.[27]. In Massachusetts, the distinction between the mortgage and the note is important because requirements for assigning the mortgage are dictated by property law principles, while the requirements for transferring the note are dictated by Uniform Commercial Code (“UCC”) principles.[28]

Accordingly the originator must fulfill certain requirements in order to properly assign the mortgage and indorse the note. First, the Statute of Frauds dictates that contracts relating to land, including assignments of mortgage, must be in writing.[29] Moreover, when challenged, the foreclosing entity must produce a properly indorsed note to assert ownership of the mortgage.[30] In practice, however, the foreclosing entity may not be able to produce sufficient evidence of its ownership of the mortgage.[31] Thus, an effective consumer law practitioner should carefully evaluate the documentation produced by the lender to determine if the lender fulfilled the requirements for a valid transfer of ownership.”

Accordingly the originator must fulfill certain requirements in order to properly assign the mortgage and indorse the note. First, the Statute of Frauds dictates that contracts relating to land, including assignments of mortgage, must be in writing.[29] Moreover, when challenged, the foreclosing entity must produce a properly indorsed note to assert ownership of the mortgage.[30] In practice, however, the foreclosing entity may not be able to produce sufficient evidence of its ownership of the mortgage.[31] Thus, an effective consumer law practitioner should carefully evaluate the documentation produced by the lender to determine if the lender fulfilled the requirements for a valid transfer of ownership.”

[Emphasis added]

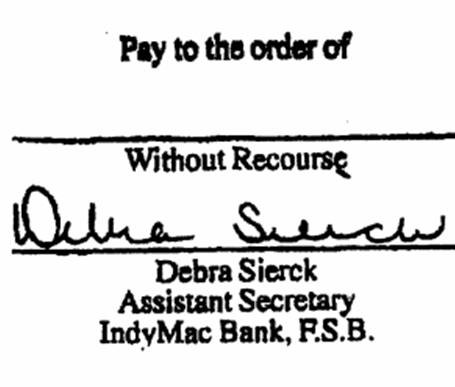

Let’s stop here for a moment and examine documents. What’s the first thing to look for? Answer: The Promissory Note FROM THE LENDER/SERVICER.

The reason for wanting the Note directly from the lender or servicer deals with the indorsements, or endorsements as the case may be.

The reason for wanting the Note directly from the lender or servicer deals with the indorsements, or endorsements as the case may be.

- Are there any endorsements on the face of the note?

- Is there an allonge? (likely undated which should be corrected by every legislature in the country for starters – make it a law that the allonges must be dated when signed)

The first question for any homeowner considering hiring an attorney to represent them in a foreclosure complaint is: “How well do you know the UCC statutes?” Because you’re going to be spending a lot of money on some guy to represent you in court and if he can’t tell you the difference between Article 3 and Article 9 – or he hasn’t read Article 8… run like hell and find another attorney. If an attorney cannot articulate the difference to you in layman terms – chances are he cannot argue it adequately to the judge.

Negotiable and non-negotiable instruments are very complex issues. Mental recall of the UCC statutes (all of them dealing with promissory notes) is essential. UCC statutes for each state and the Federal code can be found on the Internet. It is advisable, as a homeowner and borrower to read them – even if you are not in foreclosure – yet.

Negotiable and non-negotiable instruments are very complex issues. Mental recall of the UCC statutes (all of them dealing with promissory notes) is essential. UCC statutes for each state and the Federal code can be found on the Internet. It is advisable, as a homeowner and borrower to read them – even if you are not in foreclosure – yet.

Knowing exactly where your loan is right now – is crucial, because you don’t know who you are paying unless you know who is holding your loan. And there are way too many cases where we have found that Bank of America, for example, claims it own the loan – only to find out that the loan is actually actively trading in a trust – which means if it were transferred properly, the Certificate-holders should be the rightful owners.

NOW, consider this: If your loan is actually actively trading in the trust – maybe even in several tranches – how could it be a negotiable instrument? Won’t the Note/Loan be considered a security? If so, and it is actively trading – wouldn’t we be looking at a “non-negotiable” instrument? And if it is a “non-negotiable” security – would it fall under Article 9? And to get to Article 9 – isn’t the gateway through Article 8 (?) which says:

“8-501 (d) If a securities intermediary holds a financial asset for another person, and the financial asset is registered in the name of, payable to the order of, or specially indorsed to the other person, and has not been indorsed to the securities intermediary or in blank, the other person is treated as holding the financial asset directly rather than as having a security entitlement with respect to the financial asset.”

This Rule is carefully crafted and fully articulated, and it incorporates precisely the parameters necessary to obtain holder status. Now, go back and look at your Promissory Note FROM YOUR LENDER/SERVICER… Endorsed in blank? Where’s your loan? In a trust? Hmmmm…. you can see where this is heading!

Ms. Rehrauer’s paper is worth reading or re-reading. Here we are 2 Christmas’ and a Presidential election later and George Bailey is still missing… it’s as though we’re still in the chapter as if George had never been born…

Ms. Rehrauer’s paper is worth reading or re-reading. Here we are 2 Christmas’ and a Presidential election later and George Bailey is still missing… it’s as though we’re still in the chapter as if George had never been born…

“CLARENCE: Oh, I – I’m really going down to Earth, sir? Oh, how splendid.

JOSEPH: Yes. There’s a very discouraged man down there, Clarence. George Bailey. At exactly ten forty-five PM, Earth time, he’ll be thinking seriously of ending his life.

CLARENCE: Oh, dear, dear. His life.

JOSEPH: Now, I want you to stop him if you can. Now, sit down, sit down. I’ll give you Bailey’s case history.

CLARENCE: Sir, if, er … if I should accomplish my mission… may I perhaps get my wings? I’ve been waiting over two hundred years now and, well, people are beginning to talk.”

Maybe President Obama needs a “Clarence” of his own who needs a set of wings…

__________________________

Go to the LIBRARY on DOCTEL PORTAL for PDFs of the Reference Documents:

[3] See Christopher L. Peterson, Predatory Structured Finance, 28 Cardozo L. Rev. 2185, 2186-87 (2007).

[4] Id. at 2188.

[5] Id.

[23] See generally In re Hayes, 393 B.R. 259 (D. Mass. 2008); see also In re Schwartz, 366 B.R. 265, 269 (D. Mass. 2007).

[24] See generally U.S. Bank National Assoc. v. Ibanez, Nos. 08 MISC 384283, 08 MISC 386755, 2009 WL 3297551 (Mass. Land Ct. Oct. 14, 2009) (refusing to “remove a cloud from the title” pursuant to Mass. Gen. Laws ch. 240, § 6 on several homes purchased after foreclosure due to defects in assignment of mortgage).

[25] See Ibanez, 2009 WL 3297551 at *10.

[26] See Kluge v. Fugazy, 536 N.Y.S.2d 92, 93 (N.Y. App. Div. 1988) (finding that “absent transfer of the debt, the assignment of the mortgage is a nullity”); see also Robert L. Marzelli & Elizabeth S. Marzelli, Massachusetts Real Estate 2d § 5.1 (Lexis 2003) (stating that “[p]rior to instituting foreclosure proceedings it is wise to examine the note and the mortgage”).

[27] See In re Nosek, 386 B.R. 374, 380 (Bankr. D. Mass. 2008) (citing In re Schwartz, 366 B.R. 265, 270 (Bankr. D. Mass. 2007)), aff’d in part and vacated in part, 406 B.R. 434 (D. Mass. 2009); see also Ibanez, 2009 WL 3297551 at *11.

[28] See generally Ibanez, 2009 WL 3297551 (refusing to recognize an assignment “in blank” as a valid assignment, despite the fact that an indorsement in blank is a valid method to transfer a note).

[29] See Mass. Gen. Laws ch. 259, § 1 (2004); see also Adams v. Parker, 78 Mass. (12 Gray) 53 (1858).

[30] See Kluge, 536 N.Y.S.2d at 93.

[31] See, e.g., In re Schwartz, 366 B.R. 265 (Bankr. D. Mass. 2007); In re Hayes, 393 B.R. 259 (Bankr. D. Mass. 2008); In re Maisel, 378 B.R. 19 (Bankr. D. Mass. 2007).

Happy Holidays!

Reblogged this on Deadly Clear and commented:

Worth remembering.