Homewreckers: How a Gang of Wall Street Kingpins, Hedge Fund Magnates, Crooked Banks, and Vulture Capitalists Suckered Millions Out of Their Homes and Demolished the American Dream by Aaron Glantz

“In an alternate reality, the one progressives wanted, the government wouldn’t have bailed out the banks during the 2008 crash. When mortgage-backed securities began catching flame like newspaper under logs, the government would have prioritized struggling homeowners instead. It would have created a corporation to buy back the

distressed mortgages and then worked to refinance those mortgages—lowering monthly payments to reflect the real underlying values of the homes or adding years to the mortgages to make the monthly payments more manageable. If a homeowner missed mortgage payments, rather than initiating a foreclosure after two months, as was done by many banks during the recession, the government would have held off for an entire year, maybe more. In the event the homeowner still couldn’t keep up, the government would have acquired the home, fixed it up, and rented it out until another person bought it.”

[Sydney] But that didn’t happen and the alleged “Progressive” took unprecedented action against homeowners with the fake HAMP program designed for the banks – not American Homeowners – and 45 million families lost their homes, retirement, investments to foreclosures, short sales, walkaways – a death of great magnitude.

“Who could ever dream up such wild ideas? Franklin Delano Roosevelt, for one. To stanch foreclosures during the Great Depression, FDR created the Home Owners’ Loan Corporation (HOLC), which bought more than a million distressed mortgages from banks and modified them. When modification didn’t work, it sold the foreclosed homes—200,000 of them—to individuals. While the program was costly, in the end it pretty much paid for itself: because homes weren’t dumped on the market all at once, they almost always sold for close to the amount of the original loan. The New Deal—which also created the Federal Housing Administration (FHA), to guarantee mortgages with banks, and the US Housing Authority, to build public housing—inaugurated the golden era of homeownership and middle-class prosperity. It wasn’t without significant problems—the HOLC invented redlining, only providing FHA-backed loans to white people purchasing in white neighborhoods—but if you were white, this was a stabilizing and egalitarian response that held speculators at bay.

Homewreckers, Aaron Glantz’s recent book about the investors who exploited the 2008 financial crisis, is essential reading as we plunge headlong into a new financial catastrophe.” (Read MORE)

Comments below by Sydney Sullivan:

Unfortunately, as we all know now – HAMP was a crooked scam that foamed the runway for the banks. These flawed financial products were never intended to be long term mortgages. These transactions were Non-Traditional Mortgage securities – property and homeowners were plopped into a securitization/rehypothecation trafficking plan.

Servicers convinced American Homeowners that they needed to miss 3-4 payments in order to qualify for this government sponsored and well-advertised HAMP program and then promptly defined homeowners in default and began foreclosure.

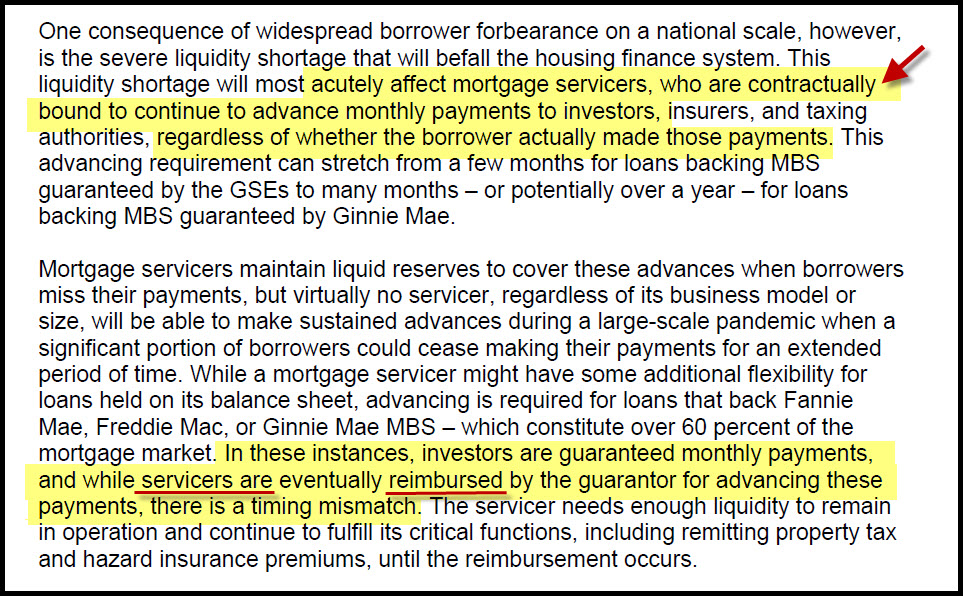

Many homeowners have been fighting to keep their homes since 2008 – recognizing the corruption that lingers in our Licensed to Lie legal system. And as luck would have it, the Mortgage Bankers Association finally [inadvertently] admitted on March 22, 2020 – after 12 years of bank servicers lying to homeowners, the courts, the media and their own bar members – that the debt was being paid – so injury to anyone or specifically who is questionable. It certainly wasn’t the plaintiffs.

Many homeowners have been fighting to keep their homes since 2008 – recognizing the corruption that lingers in our Licensed to Lie legal system. And as luck would have it, the Mortgage Bankers Association finally [inadvertently] admitted on March 22, 2020 – after 12 years of bank servicers lying to homeowners, the courts, the media and their own bar members – that the debt was being paid – so injury to anyone or specifically who is questionable. It certainly wasn’t the plaintiffs.

That goes to the original question from years back – “Can my Uncle Sam pay my mortgage for me?” The IRS answer was, “Yes, as long as neither of you claimed a mortgage deduction for the amount.”

More on this subject later.

![]()