By Sydney Sullivan

Shortfall. Unfunded. Underfunding. Sounds like a minimal pension issue – however, it is anything but that. You may have heard the words “shortfall” when your state refers to it’s government budget or pension plan; and, if you are young (say, under 40), you’ve probably not given it a second thought. Just so you know “shortfall” is defined as “a failure to come up to expectation or need” and at 40 it seems like there will be plenty of time and ways to make up a shortfall… not so much when you are 60.

Shortfall. Unfunded. Underfunding. Sounds like a minimal pension issue – however, it is anything but that. You may have heard the words “shortfall” when your state refers to it’s government budget or pension plan; and, if you are young (say, under 40), you’ve probably not given it a second thought. Just so you know “shortfall” is defined as “a failure to come up to expectation or need” and at 40 it seems like there will be plenty of time and ways to make up a shortfall… not so much when you are 60.

If you’re like many Americans, you’re worried about retirement. Maybe before the new century securitization scheme was launched, a “shortfall” might have been more easily explained and handled. But after 2000, the Wall Street securities system ramped up and took deficits to a new high while lining the pockets of Wall Street traders. How did this happen?

How did the USA get to over $3.4 TRILLION in unfunded pension debt? The answer is not something your Congressional or state legislators want to discuss in public …or even in confidence. What caused “shortfalls”? To understand how a state could get so severely “underfunded” with their pension funds, you must first understand that this didn’t just happen overnight. De-regulation and rule changing has been going on since the last Great Depression, though the final wallop occurred when Congress repealed Glass-Steagall in 1999. “Glass-Steagall was designed to prevent exactly the kind of collaboration that brought us the Goldman-Sachs fraud.” Source: Daily Kos.

Now, a lot of people blame a Republican Congress under the Clinton administration for the demise of Glass-Steagall – however, that is not altogether true. The House Democrats were instrumental in passing the repeal – even Nancy Pelosi (whose husband worked for Countrywide) voted “yea”. Sad fact, but true. We all make mistakes as both the parties agreed it was best to reinstate Glass-Steagall – at least as far as their party platforms go.

Check the record … how did your own Senators and Congresspersons vote?

Senate Vote: http://www.govtrack.us/…

House Vote: http://www.govtrack.us/…

How is this related to underfunded pensions? “Glass-Steagall was repealed in 1999 by then President Bill Clinton and a Republican-controlled Congress who pushed for the passage of the Gramm-Leach-Bliley bill. Gramm-Leach-Bliley was named after its three sponsors, all of them Republicans: Congressmen Phil Gramm (R-Texas), Jim Leach (R-Iowa) and Thomas J. Bliley, Jr. (R-Virginia). The Gramm-Leach-Bliley Act tore down the regulatory framework that would have helped protect against the sub-prime mortgage bubble and the speculation that led to a collapse of the market where speculators traded the “derivative” securities that were created from those sub-prime mortgages.” Source: Daily Kos. None of these fellows are sitting in our Congress today, thankfully.

And who invested (or was solicited to invest) in those unregulated derivatives consisting of mortgage-backed securities, asset-backed securities and auction rated securities (school loans)? Unions and corporate pension funds. Billion$, if not Trillion$, of dollars poured into investment banks – anxious to gamble money in risky derivatives and make up earlier shortfalls.

For example, West Virginia teachers had experienced problems. “While teachers had always made their contributions (6% of their pay out of every paycheck), the state and many county school boards failed to make their full contributions for many years. In fact, for some years from 1979 onward, the state and many school boards failed to match even employee contributions to the fund.” Source: National Institute on Retirement Security.

Fast forward to 1999 – the securitization Casino opened. Come one, come all! Who knows besides the agents or fund managers exactly what was promised – but suffice to say – the monies were lost, sometimes rapidly – in a system “designed” to crash. Was it intentional – hard to say. Did it intend to eliminate unions? Again, hard to say. But, to some degree, it did. The unions became more vulnerable – because they too believed that the Wall Street “system” was legitimate – when it was actually rigged – from appraisals to LIBOR…and beyond.

Who rigged the system? Well, it wasn’t the homeowners. It wasn’t the students and it wasn’t the credit card borrowers. What is really funny, is that the “system” is a complex computer software driven vehicle. It appears, the data inside the system is weaponized to create destruction. Why else would upstanding homeowners be paired off by robot computers in a securitized trust with derelicts that had no credit and could barely breathe?

The Wall Street (best money can buy) computer system is intelligent – the USPTO patented computer platform systems claim to be able to detect fraud – yet they apparently were not working or were “relaxed” (as many pension fund lawsuits claim) when they funded “stated income” loans. It appears the computer systems used “expert reasoning” algorithms in their design. All for one – and one for all. YBG-IBG.

Bottom-line is that this entire chaos consisting of over $3.4 TRILLION [$3,400,000,000,000] dollars – underfunded, will affect retirees that have worked all their lives (and in many cases risked their lives) expecting to receive a pension that will no longer be there.

A top story – America’s Horrible Pension Underfunding Debacle. Congress (the culprits) quietly passed and President Obama signed into law the 2015 Omnibus spending bill, which includes provisions that allow trustees of certain multiemployer plans to cut retirees’ pensions.

Here is a summary of these provisions:

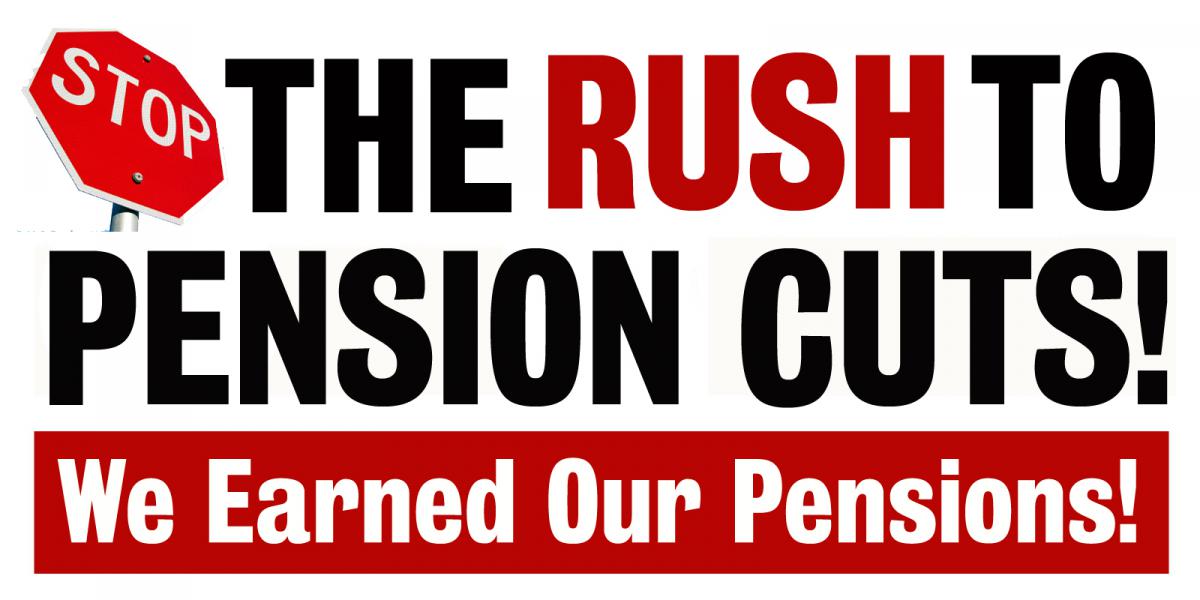

- The legislation permits deep pension cuts to retirees in certain financially-troubled multiemployer plans. Financially-troubled plans are plans expected to not have enough money to pay 100% of benefits within 15 and, in some cases, 20 years.1 There are instances where the cuts could be more than 60% of a participant’s benefits. To find out how much your benefits could be cut use this calculator.

- The decision to cut benefits is made by plan trustees, who are typically more aligned with active workers and employers than with retirees.

- Retirees who are age 80 or over, or who are receiving a disability pension, are not subject to benefit cuts. Retirees ages 75-79 are subject to smaller cuts than retirees under age 75.

- How big or small the cuts are for those under age 75 is determined by the trustees. The cuts are subject to certain legal limits, the most important of which is that benefits cannot be cut below 110% of the amounts that the federal pension insurance agency guarantees. Read more HERE.

More legislation is being considered because the pension deficits threaten the stability of the states and municipalities. Do we see Congressional, Judicial or legislative pension haircuts? Kentucky, for example, is reeling with underfunded pensions with only 17.7% to pay its retirees.

“Pending are vast changes to Social Security rules included in the House 2015 Budget, which is being rushed through Congress without any hearings or time for public comment.

The bill will reduce the lifetime benefits of millions of Americans by tens of thousands if not hundreds of thousands of dollars. It will do so, in large part, by inducing people to take their retirement benefits far too early in order make up for the loss of spousal, divorce(e) spousal, child, disabled child, excess widow(er) and excess divorce(e) widow(er) benefits. Source: PBS.org

The bill not only cuts benefits for people who are about to make their Social Security collecting decisions, but it also stops benefits that people are already collecting. This is an absolutely terrible precedent for Congress (and the administration, which is fully on board) to make. No retiree will ever again be able to feel their Social Security benefits are safe from some backroom, midnight, rushed change in rules that are designed to meet some budget target or accommodate some politician’s whims.”

This isn’t new. This has been quietly eroding your retirement funds (and/or union) well before 2008 when the USA economy crashed – and remember your Congressional representatives (above) voted to repeal the protection of Glass-Steagall. One has to wonder if Congress knew pensions were dangerously underfunded, how could they approve any additional spending or changes in certain protective Acts until such deficits were taken care of?

If you pay money into a pension fund and it disappears, and you didn’t know the fund was gambling your money (no disclosure) – well, isn’t that ahhh…concealment? Sure, maybe you could have asked how the funds were being handled. Maybe you could have investigated a little more – but really, if you think you are putting money away for the future – who really has the right to gamble with it – without telling you? Wouldn’t it seem a bit unethical?

Should we assume our Congressional leaders and legislators don’t understand the risky mechanism for the loss of pension funds? That would make them a bit naive – and nevertheless not fit for office. But don’t you think they could find a creative new way to re-fund the pension deficits – if this wasn’t intentional?

Okay, pension and retirement funds were invested in risky unregulated derivatives – the sale of unregulated securities. That should be the first bone to pick.

- State pension funds

should not be allow to invest in anything unregulated (Congress may have corrected that by now).

should not be allow to invest in anything unregulated (Congress may have corrected that by now). - Second, pension funds should only be taxed when the custodian gambles with them – no need for some REMIC scheme to park money.

- Third, mandatory full disclosure should be made to ALL parties, including homeowners, that this is securities transaction and exactly who the beneficiaries are from the very beginning – not through “discovery.” This is elementary if Congress really wants to clean up the system.

And fourth, if there are to be any haircuts, especially in social security – they should go all the way to the top. Congress and the judiciary receive the same pension haircuts as the people they work for. Level the playing field.

And finally, how would you refund the pension systems? One reader suggested a special lottery where all the proceeds filtered directly to the pension accounts and no where else until the coffers were full. Another reader suggested a pension tax on all alcohol, marijuana and cigarettes. One of the most dynamic suggestions was a tax on war. Anything dealing with war-related legislation and industry (including building nuclear energy plants) would be taxed and divided up among the states to replenish their pension systems.

The most favorable plan – each state take possession of the foreclosures in their state. We’re getting nowhere with modifications. The banks, it appears, have already collected non-recourse insurance – THEY HAVE BEEN PAID. So, states need to retake their lands through a state agency – and either renegotiate with the homeowners (screwed by the HAMP program or the banks) or sell the properties and refund the pension system.

Look at it this way: 50,000 homes X $900 a month (conservative) is $540 million dollars of new revenue a year. In ten years that’s conservatively $5,400,000,000 (billion) replenishing the pension funds without added investing. And in what state did the banks do less than 50,000 mortgages?

Courts Are Taking Notice as outlined by Ellen Brown, Web of Debt in 2012:

“The title issues are so complicated that judges themselves have been slow to catch on, but they are increasingly waking up and taking notice. In some cases, the judge is not even waiting for the borrowers to raise lack of standing as a defense. In two cases decided in New York in December, the banks lost although their motions were either unopposed or the homeowner did not show up, and in one there was actually a default. No matter, said the court; the bank simply did not have standing to foreclose.

Failure to comply with the terms of the loan documents can make an even stronger case for dismissal. In Horace vs. LaSalle, Circuit Court of Russell County, Alabama, 57-CV-2008-000362.00 (March 30, 2011), the court permanently enjoined the bank (now part of Bank of America) from foreclosing on the plaintiff’s home, stating:

[T]he court is surprised to the point of astonishment that the defendant trust (LaSalle Bank National Association) did not comply with New York Law in attempting to obtain assignment of plaintiff Horace’s note and mortgage. . . .

[P]laintiff’s motion for summary judgment is granted to the extent that defendant trust . . . is permanently enjoined from foreclosing on the property . . . .

Relief for Counties: Land Banks and Eminent Domain

The legal tide is turning against MERS and the banks, giving rise to some interesting possibilities for relief at the county level. Local governments have the power of eminent domain: they can seize real or personal property if (a) they can show that doing so is in the public interest, and (b) the owner is compensated at fair market value.

The public interest part is obvious enough. In a 20-page booklet titled “Revitalizing Foreclosed Properties with Land Banks,” the U.S. Department of Housing and Urban Development (HUD) observes:

The volume of foreclosures has become a significant problem, not only to local economies, but also to the aesthetics of neighborhoods and property values therein. At the same time, middle- to low income families continue to be priced out of the housing market while suitable housing units remain vacant.

The booklet goes on to describe an alternative being pursued by some communities:

To ameliorate the negative effects of foreclosures, some communities are creating public entities — known as land banks — to return these properties to productive reuse while simultaneously addressing the need for affordable housing.

States named as adopting land bank legislation include Michigan, Ohio, Missouri, Georgia, Indiana, Texas, Kentucky, and Maryland. HUD notes that the federal government encourages and supports these efforts. But states can still face obstacles to acquiring and restoring the properties, including a lack of funds and difficulties clearing title.”

Once obtained by the state, Quiet title and “state mortgage” the property. Use the funds generated from the “take back” to replenish the pension funds. Make the monies untouchable by future legislators.”

All in all we need to protect the retirees. These are our firemen, police, school teachers, government employees …not to forget our judges, clerks, aides and legislators who have worked for the benefit of our communities expecting to someday themselves to be able to retire.

The funds were gambled away – now well beyond their control – and Congress should not be allowed to just wash that time and investment away, lest they wash away their own investments first.

Thank you for this great Blog. In your Blog dated August 26, 2013, about the New York Trust Law, my question is: does the Act EPTL 7-2.4 still active?, Because I have been hearing that it is not a ‘good law’ any longer. I will truly appreciate your answer. and if you have any updated recent cases to support that it is still a ‘good law’

Pingback: Securities Fraud: In Search of the Holy Grail of Foreclosure Defense | Deadly Clear

Pingback: Are Good Foreclosure Defense Attorneys an Endangered Species? | Deadly Clear

Pingback: Are Good Foreclosure Defense Attorneys an Endangered Species? – rogerrinaldi

Pingback: Hawaii State Public Funds’ Shortfall Hits $25B | Deadly Clear

Reblogged this on Deadly Clear and commented:

People are wondering why unions are dwindling – it’s because of the securitization/rehypothecation scheme targeted unions to invest in their UNREGULATED DERIVATIVES,.while Congress has done nothing to stop it. Union busting? Globalism? Agenda 21?

Pingback: The Securitization Debacle – A U.S. Pension Shortfall: $3.4 Trillion+ [$3,400,000,000,000] | Deadly Clear

Pingback: Hawaii union members hold news conference to discuss taking legal action against COVID vaccine mandate | Deadly Clear