By Sydney Sullivan

Four astounding men, Gary Aguirre, Bill Black, Richard Bowen, and Michael Winston, are the founding members of the Bank Whistleblowers United. These well-educated men have the moral integrity and intelligence to see the damage Wall Street has caused and have devised a plan to prevent or at least reduce the frequency and harm of future economic crises.

Four astounding men, Gary Aguirre, Bill Black, Richard Bowen, and Michael Winston, are the founding members of the Bank Whistleblowers United. These well-educated men have the moral integrity and intelligence to see the damage Wall Street has caused and have devised a plan to prevent or at least reduce the frequency and harm of future economic crises.

We, as American citizens, know we have not recovered from the 2008 economic crisis as our present administration and Congressional leaders would like for us to believe. Although lots of warriors have stepped up to battle the banks, none have been as united or noteworthy as these four financial fraud-busting astronauts, venturing into a red banking hole existing in cyberspace which has been an arduous climb up-Hill (pun intended) to penetrate, decipher …and even more difficult to correct.

Their 60-day plan, described in detail below, is ingenious. It would be difficult for anyone in foreclosure defense or fighting the derivatives securities scam not to fully embrace the efforts and help create the momentum needed to push the objectives forward.

While the financial crisis affects all Americans, young and old, it’s hard for average folks to understand the gravity of the situation. All they know is that they can’t make ends meet. It didn’t have to be like this – but until our government decides to assume some moral integrity the majority of citizens will continue to suffer – for something that was not their/our fault.

While the financial crisis affects all Americans, young and old, it’s hard for average folks to understand the gravity of the situation. All they know is that they can’t make ends meet. It didn’t have to be like this – but until our government decides to assume some moral integrity the majority of citizens will continue to suffer – for something that was not their/our fault.

It doesn’t matter what your political views are, as politics has become another divisive measure in America to pit neighbor against neighbor, brother against brother and the end result affects all of us …and our children …and our grandchildren.

Writing this post in order to reach beyond the academics of the message so we could all understand how immeasurably important it is for a solid movement, initiative, message, agenda (or whatever you want to call it) – was somewhat perplexing given the nature of this complex financial corruption. While flipping through the TV channels – and again, please leave the archaic, dividing and propagandized politics out of your thought process and listen to the message – Ron Paul had an interesting infomercial. Stopping on the channel to listen was the message so many of our leading economists have been trying to tell America. In addition, Dr. Paul explains the perils of trying to work in Congress. Whether you like him or not – there is a message here that should concern you. We ARE on the verge of another collapse.

Bill Black is an Associate Professor of Economics and Law at the University of Missouri – Kansas City (UMKC) and the Distinguished Scholar in Residence for Financial Regulation at the University of Minnesota Law School and leads our four gentlemen in getting the message across.

Bill Black is an Associate Professor of Economics and Law at the University of Missouri – Kansas City (UMKC) and the Distinguished Scholar in Residence for Financial Regulation at the University of Minnesota Law School and leads our four gentlemen in getting the message across.

“The most recent U.S. bubble and resultant financial crisis and Great Recession were driven by three epidemics of fraud led by elite bankers. The three epidemics that drove the crisis are appraisal fraud, “liar’s” loans (collectively, these were the loan origination frauds), and the resale of those fraudulently originated mortgages through fraudulent “reps and warranties” to the secondary market and the public. Banks, like fish, rot from the head – the “C Suite.” Liar’s loans is an industry term that shouts the industry’s knowledge that it was originating overwhelmingly fraudulent loans. In a liar’s loan the lender agrees not to verify data that is essential to prudent underwriting. This would be an insane practice for an honest lender – and it was practice that was always discouraged by the federal regulators – but it optimizes “accounting control fraud.””

We’ve posted extensively about the software patents used by the banks that have numerous safeguards designed to catch and protect against fraud. The software was also designed to relax those safeguards and intentionally invite fraud – almost as a human experiment designed by well-engineered algorithms. Yes, the software devised the liar’s loans and there is no way that the banks were not aware of their intended malice.

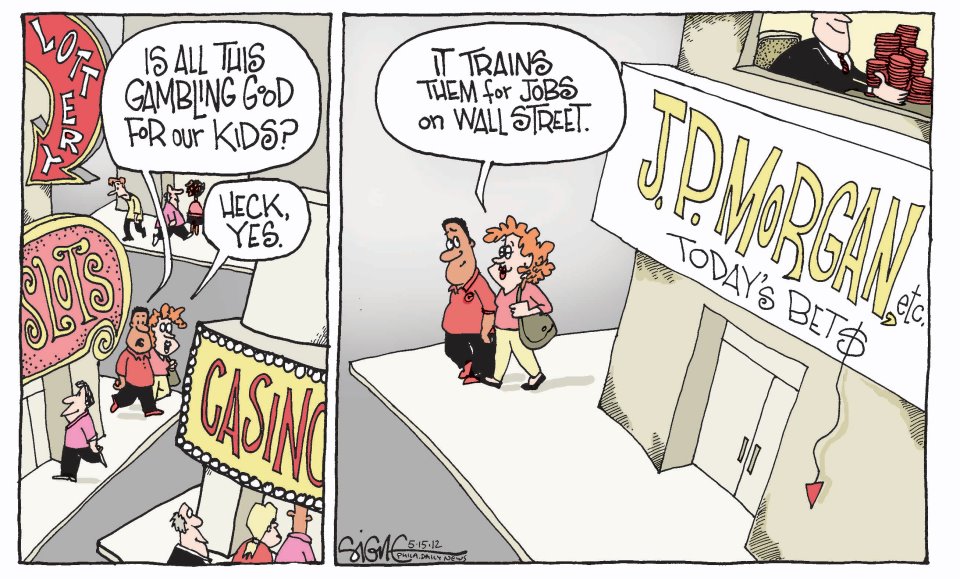

Homeowners were targeted in a sophisticated arena never knowing they were gambling on Wall Street – as there was no disclosure.

Homeowners were targeted in a sophisticated arena never knowing they were gambling on Wall Street – as there was no disclosure.

However, there were pre-existing agreements between the pretender lenders and the investment banks (underwriters) that procured the homeowner collateral for the purpose of securitization – it appears it was a securities transaction – with no disclosure which would have violated Rule 10b-5 of the SEC.

Prof. Black and his posse report that, “[O]ur group is predominately former bankers who worked at fairly senior levels for enormous financial institutions. We do not hate banks or bankers as a group. We know, however, that when elite fraud is not stopped by the regulators and the prosecutors it is likely to create a “Gresham’s” dynamic. The Nobel Laureate George Akerlof was the first economist to describe this dynamic in 1970.

“[D]ishonest dealings tend to drive honest dealings out of the market. The cost of dishonesty, therefore, lies not only in the amount by which the purchaser is cheated; the cost also must include the loss incurred from driving legitimate business out of existence.”

We can confirm Akerlof’s warnings about fraud. Indeed, we can testify from personal knowledge that when bad ethics is encouraged it will over time tend to drive good ethics out of individual firms. Fraudulent senior bankers deliberately create a Gresham’s dynamic within the firm and in hiring “independent” professionals in order to drive honest employees out of the bank and to suborn outside professionals that are supposed to act as external “controls” to serve instead as fraud enablers.

We can confirm Akerlof’s warnings about fraud. Indeed, we can testify from personal knowledge that when bad ethics is encouraged it will over time tend to drive good ethics out of individual firms. Fraudulent senior bankers deliberately create a Gresham’s dynamic within the firm and in hiring “independent” professionals in order to drive honest employees out of the bank and to suborn outside professionals that are supposed to act as external “controls” to serve instead as fraud enablers.

At places like Countrywide, thousands of employees left annually because they refused to abuse their customers. Only by restoring the rule of law to Wall Street can we allow honest banks and honest bankers to dominate Wall Street.”

The Whistleblowers United 60-Day Plan:

- Restore the mandatory criminal referral process and Criminal Referral Coordinators at every financial regulatory agency

- Require that all new hires agree to conditions that will end the “revolving door” – with no provision for waivers.

- The FBI and the Department of Justice (DOJ) will publicly terminate their “partnership” with the Mortgage Bankers Association – the industry trade association which has a clear conflict of interest and harms prioritization by pushing solely for the prosecution of what should be far lower priority cases of crimes v. banks and never for the prosecution of what should be the highest priority cases of frauds led by banks’ senior officers

- Ban DOJ from making deferred prosecution agreements with elite white-collar criminals

- Reassign 500 FBI agents to the white-collar crime section

- Request authority from Congress to hire 3,000 FBI agents, 250 DOJ attorneys, 250 SEC investigators and enforcers. This is the only portion of our plan requiring legislation.

- Stop prosecuting the mortgage fraud “mice” and use all DOJ and FBI resources against the fraud “lions”

- Rescind the FBI’s false claim on its web site that asserts:

“Ethnic groups involved in mortgage loan origination fraud include North Korean, Russian, Bulgarian, Romanian, Lithuanian, Mexican, Polish, Middle Eastern, Chinese, and those from the former Republic of Yugoslavian States.”

This false ethnic claim, again, leads the FBI to prioritize the fraud “mice” rather than the “lions.”

- Prioritize FBI and DOJ resources by creating a “Top 100” list of the worst financial fraud schemes

- Revamp the federal treatment of whistleblowers and False Claim Act complainants to encourage their efforts and use them to hold financial elites personally accountable

- Make public a list of exemplary financial whistleblowers and set forth in writing what they have done for the Nation. (The President should, of course, do this for whistleblowers in each field, not just finance.)

- The President should hold a public event at which he or she presents appropriate awards in person to these exemplary whistleblowers. We are not talking about financial awards and we are willing to be excluded from consideration for these Presidential awards lest we be charged with self-aggrandizement.

- Review the backlog of whistleblower and False Claims Act complaints with fresh eyes committed to finding any useful source of information to assist in deciding whether to bring enforcement, civil, or criminal actions against elite financial frauds.

- Make public the Clayton reports on secondary market sales. These reports document pervasive secondary mortgage market fraud.

- Federal banking regulators will:

- Impose individual minimum capital requirements (IMCR) for all systemically dangerous institutions (SDIs) commensurate with the risk they pose because of their size

- Impose IMCRs for all SDIs commensurate with the risk they pose because of their non-commercial bank activities

- Impose IMCRs for all banks commensurate with the risk posed by their executive compensation systems

- Impose IMCRs for all banks commensurate with the risk posed by their hiring, retention, and compensation systems for purportedly independent professionals such as outside auditors, appraisers, and credit rating agencies

- Announce that it is the policy of the United States never to engage in a regulatory “race to the bottom” with any other government

- Direct each major federally regulated bank to conduct and publicly report a “Krystofiak” study on samples of “liar’s” loans that they continue to hold. Krystofiak studies quantify the extent of loan origination and secondary market fraud by lenders.

- Appoint new, vigorous heads of each federal financial regulatory agency

- Promptly train federal banking and securities regulators, the FBI, and DOJ on sophisticated fraud schemes, particularly fraud via accounting

- End the use of deliberately unenforceable financial regulatory “guidelines””

The question for every political candidate is:

Will You Support the Whistleblowers’ First 60-Day Pledge?

Will You Support the Whistleblowers’ First 60-Day Pledge?

And so we ask each presidential candidate – which portions of the Whistleblowers’ 60-Day plan will you pledge to implement? We hope the candidates will commit to breaking Wall Street’s power over our economy and democracy.

The Whistleblowers’ 60-Day plan provides any candidate with the practical steps necessary to make real the twin goals of restoring the rule of law to Wall Street and ending crony capitalism.

Our goal is to offer constructive, realistic means by which the next President can achieve these twin goals.

![]()

Associated Documents (click on the links):

Who Are We?

Bio: Gary Aguirre

Bio: William K. Black

Bio: Richard Bowen

Bio: Michael Winston

BTW – In the process of researching we found: Change your synonyms for whistleblower directed to Merriam-Webster/Thesaurus.com and quite agree. “Here are several synonyms that more honestly and accurately describe whistleblowers: watchdog, truthteller, and fraud-buster. We ask that you replace your current whistleblower synonyms with these and other terms more befitting the true character and contributions of whistleblowers.”

Excellent article Deadly Clear – can we get Black to talk more about this??

Reblogged this on Justice League.

Giving perhaps more pointed detail than Dr. Paul, briefly, here is a nice little presentation by Dr. E Vieirra to the Rotary Club of New York in 2003, “Trashing the Constitution: How misconstruction of the monetary powers and disabilities subverted the Founding Fathers’ intent.”

http://www.constitution.org/mon/vieira_03225.htm