While fishing for bank-related patents this gem surfaced and jumped into the net. At first it wasn’t apparent it was a keeper because the UETA issue has not been in the forefront of foreclosure defense. However, taking the time to dissect the document it became apparent that, as some of us have suspected, there is a mandatory methodology from the origination of the mortgage loan on a trip to the securitized trust that includes the EXPLICIT CONSENT of the obligor (homeowner).

While fishing for bank-related patents this gem surfaced and jumped into the net. At first it wasn’t apparent it was a keeper because the UETA issue has not been in the forefront of foreclosure defense. However, taking the time to dissect the document it became apparent that, as some of us have suspected, there is a mandatory methodology from the origination of the mortgage loan on a trip to the securitized trust that includes the EXPLICIT CONSENT of the obligor (homeowner).

Yup… It appears the road to securitization needs an electronic record that the “issuer” aka the “obligor” has explicitly consented to at the time of origination. Yeah, ya think maybe that was the real intention of MERS aka Mortgage Electronic Registration Systems, Inc.? But it looks like it didn’t have all its ducks in a row. This is a lot to digest – but you need to know and understand this information in order to plead your case correctly before the courts.

As the third Mortgage Electronic Registration Systems, Inc. and the Trustees for the alleged REMIC trusts began filing foreclosure proceedings, fraudulent assignment of mortgages and other fabricated robo-signed documents began to surface. As a result, discussion and dissection of securitization and MERS dominated the court process.

As the third Mortgage Electronic Registration Systems, Inc. and the Trustees for the alleged REMIC trusts began filing foreclosure proceedings, fraudulent assignment of mortgages and other fabricated robo-signed documents began to surface. As a result, discussion and dissection of securitization and MERS dominated the court process.

MERSCORP, INC. executives claimed that “MERS” was created to avoid the cost of recordation at the state levels while they transferred their securitized documents about… but, it appears, that too was a misrepresentation possibly in order to avoid charges of “Fraud in the Factum.”

Fraud in the Factum is a type of fraud where misrepresentation causes one to enter into a transaction without accurately realizing the risks, duties, or obligations incurred. If this were to be the case, the entire game would be over because Fraud in the Factum usually voids the instrument under state law and is a real defense against even a holder in due course. Source: Wikipedia

The real significance of “MERS” is still not sorted out and certainly has not been adjudicated properly, primarily because attorneys and homeowners don’t dig deep enough into history of these corporations to understand the entire intent and make-up of the scam. Additionally, it appears there was an obvious attempt to confuse and intermingle the true identities of MERS. Thus, we get a hodge-podge of opinions because the judiciary can only rule on the facts as presented.

THE MYTH AND MYSTERY OF MERS IS UNVEILED

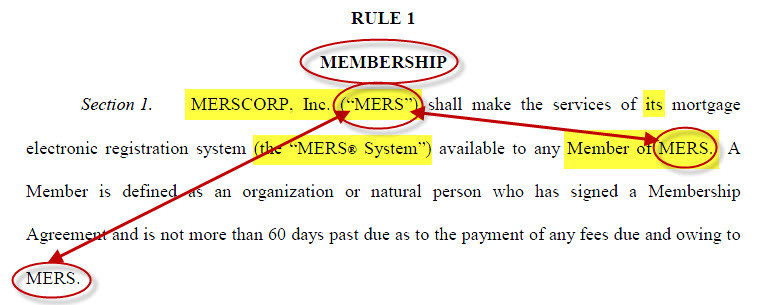

NO. 1 – MERS in the mortgages is NOT the “MERS® System” and it’s not MERSCORP, INC. Certainly, it’s time that declaratory actions are taken to determine just who is who and who is what. The very first paragraph in the MERSCORP, INC. RULES OF MEMBERSHIP [click for PDF] under Rule 1 sorts out some of the mystery if you just take the time to read it. Note it does NOT mention “Mortgage Electronic Registration Systems, Inc.” (the 3rd same name corporation):

NO. 1 – MERS in the mortgages is NOT the “MERS® System” and it’s not MERSCORP, INC. Certainly, it’s time that declaratory actions are taken to determine just who is who and who is what. The very first paragraph in the MERSCORP, INC. RULES OF MEMBERSHIP [click for PDF] under Rule 1 sorts out some of the mystery if you just take the time to read it. Note it does NOT mention “Mortgage Electronic Registration Systems, Inc.” (the 3rd same name corporation):

“Section 1. MERSCORP, Inc. (“MERS”) shall make the services of its mortgage electronic registration system (the “MERS® System”) available to any Member of MERS. A Member is defined as an organization or natural person who has signed a Membership Agreement and is not more than 60 days past due as to the payment of any fees due and owing to MERS.”

Dissect this section above before you proceed. MERSCORP, INC. (“MERS”) is the entity that makes the services of its registry system, the “MERS® System”, available to any Member of MERS, meaning members of MERSCORP, INC. – NOT the Mortgage Electronic Registration Systems, Inc. (aka MERS) that is in the mortgages.

The “MERS” acronym in the MERSCORP, INC. RULES OF MEMBERSHIP document is the acronym for MERSCORP, INC. nka MERSCORP HOLDINGS, INC.

DO NOT CONFUSE IT with the Mortgage Electronic Registration Systems, Inc. (aka “MERS“) in the mortgages – BECAUSE THEY ARE SEPARATE CORPORATE ENTITIES. Although the Mortgage Electronic Registration Systems, Inc. (aka “MERS”) in the mortgages has the same acronym (likely on purpose to be intentionally confusing) it is nothing but a shell, a straw-man, no employees, no assets, no software registry systems, no members – NO NOTHING!

See also THE 3 STOOGES OF MERS – DISORDER IN THE COURT on DeadlyClear [click for link]; and www.doctelportal.com in the Library under the MERS tab.

See also THE 3 STOOGES OF MERS – DISORDER IN THE COURT on DeadlyClear [click for link]; and www.doctelportal.com in the Library under the MERS tab.

As early as 2006, states like Florida began to seriously question the validity of the MERS in the mortgages and its ability to foreclosure. Apparently, MERSCORP, INC. recognized trouble brewing and mandated in its rules no foreclosures in the name of MERS in Florida:

“(c) In the State of Florida, the authority to conduct foreclosures in the name of MERS granted to a Member’s Certifying Officers under Paragraph Three of the Member’s MERS Corporate Resolution is revoked. Effective June 1, 2006, the Member shall be sanctioned $10,000.00 per violation for commencing a foreclosure in Florida in the name of MERS.”

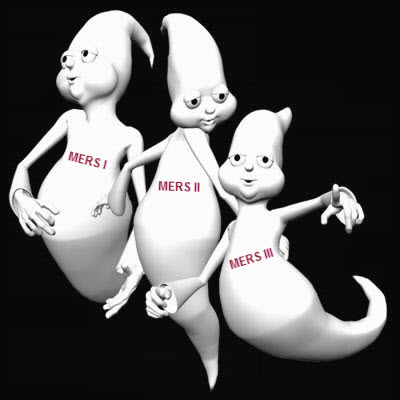

But no one was foreclosing in the name of MERSCORP, INC. in Florida in those days because MERSCORP INC. was not in the mortgages – so it appears the intentional cover-up of who the actual MERS entities were had already begun and/or maybe the entire scheme was premeditated? Especially, since there were 3 separate entities all named the same – and 4 acronyms… MERS I, MERS II, MERS III and MERS for MERSCORP, INC..

NO. 2: THE REAL PURPOSE OF Mortgage Electronic Registration Systems, Inc.

It has been a mystery how promissory notes could be materially altered and magically changed into securities to be distributed to certificate-holders in securitized trusts without the borrowers’ consent, authorization or knowledge. It wasn’t just a case of: “you signed a document allowing them to sell the loan.” Because there is more to taking a UCC Article 3 negotiable instrument and changing it into a UCC Article 9 securities for distribution.

It has been a mystery how promissory notes could be materially altered and magically changed into securities to be distributed to certificate-holders in securitized trusts without the borrowers’ consent, authorization or knowledge. It wasn’t just a case of: “you signed a document allowing them to sell the loan.” Because there is more to taking a UCC Article 3 negotiable instrument and changing it into a UCC Article 9 securities for distribution.

Apparently, as the controlling legal system was (and still is) – it appears legally the banks cannot make the change into securitization without explicit consent of an electronic record, eRegistry or eTransfer. How did we lose track or allow the mortgage process to get carried away without oversight or controls? Actually, the banks patented nearly every single move they made – even the behavioral aspects of dealing with the customers, judges, politicians, etc. as if to legitimize their scheme. Had anyone realized this 7 years ago we might have nipped the fraudclosure before it devastated the entire economy. It appears those in the securitization industry and legislatures that knew the real purpose looked the other way and intentionally concealed the truth.

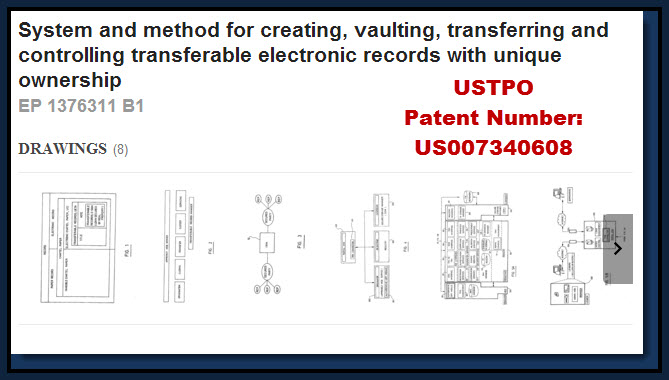

When the patent for “System and method for creating, vaulting, transferring and controlling transferable electronic records with unique ownership” [click on this link for PDF] surfaced its description included: “Field of the invention

When the patent for “System and method for creating, vaulting, transferring and controlling transferable electronic records with unique ownership” [click on this link for PDF] surfaced its description included: “Field of the invention

-

The present invention is directed to a system and method for creating, vaulting, transferring, and controlling transferable electronic records with unique ownership, such as chattel paper, notes, documents of title, and promissory notes.”

The patent extensively outlines the legal requirements for the magical change of the negotiable promissory note into securities instruments chopped up into pieces for distribution to numerous investors who were to become the “Certificate-holders” of securitized REMIC trusts:

“Legal Requirements

-

There are three primary laws that define the legal requirements for controlling ownership, rights, and obligations in financial and commercial transactions in the United States: the revised Article 9, Section 105 of the Uniform Commercial Code (UCC 9-105), Section 16 of the Uniform Electronic Transactions Act (UETA), and Title II of the Electronic Signatures in Global and National Commerce Act (E-SIGN). UCC 9-105 is a federal law that was enacted in 1998 and took effect on July 1, 2001. UETA is a uniform state law that was approved for enactment in July 1999. E-SIGN is a federal law that was enacted on June 30, 2000.”

Well, isn’t that an interesting piece of history? Anyone who has extensively studied MERS, I, II, III and MERSCORP, INC. knows that these laws were enacted at about the same time that the MERSCORP, INC. “electronic registry” and software system was created. Wasn’t that convenient? Now, this patent and others like it registered to BofA, Chase, Wells Fargo, Fannie, etc. all refer and/or incorporate the necessity of electronic transactions, registry or recordation. Thus, mortgages began pouring out with Mortgage Electronic Registration Systems, Inc. as nominee and mortgagee for the lender.

Well, isn’t that an interesting piece of history? Anyone who has extensively studied MERS, I, II, III and MERSCORP, INC. knows that these laws were enacted at about the same time that the MERSCORP, INC. “electronic registry” and software system was created. Wasn’t that convenient? Now, this patent and others like it registered to BofA, Chase, Wells Fargo, Fannie, etc. all refer and/or incorporate the necessity of electronic transactions, registry or recordation. Thus, mortgages began pouring out with Mortgage Electronic Registration Systems, Inc. as nominee and mortgagee for the lender.

It sounded like an electronic registry system, didn’t it? But “MERS III” was running into problems. It did not own or legally hold the note. It appears that MERS had split the note and the mortgage apart which was causing quite a problem in courts of foreclosure. That, however, was the least of its problem compared to the following:

- “The legal requirements as mandated in UCC 9-105, UETA Section 16, and E-SIGN Title II describe how to handle and maintain control over transferable electronic records such as electronic chattel paper and mortgage notes. Precise definitions of these terms are provided below. UCC 9-105 introduced the concept of an electronic chattel paper and set legal requirements for the control of electronic chattel paper including its assignment, in electronic form, from one party to another.” [all emphasis added by Ed. DC]

We all should [by now] understand that to get into a securitized trust the note must transform under the rules for UCC Article 9, right? If you’re lost, stop and take a break because there is more to follow that you need to understand. The patent continues:

- “UETA Section 16, referencing similar language and concepts as UCC 9-105, introduced a similar but limited concept of transferable records as electronic records that are equivalent to either paper promissory notes (i.e. negotiable instruments) or paper documents of title. E-SIGN Title II, referencing transferable records under UETA Section 16, narrowed the scope of transferable records to promissory notes that are secured by real property and allowed for the use of electronic signatures to execute such transferable records.”

Holy Aloha! The sting is in place. As long as the states adopted these new electronic eSign rules the banks had a slick path to the unregulated securitization process that it appears was set-up to glean a fortune using unsuspecting homeowners’ collateral to bait pension fund investors. UETA includes promissory notes and documents of title in its definition of transferable records. E-SIGN strictly defines transferable records as promissory notes relating to a loan secured by real property.

Holy Aloha! The sting is in place. As long as the states adopted these new electronic eSign rules the banks had a slick path to the unregulated securitization process that it appears was set-up to glean a fortune using unsuspecting homeowners’ collateral to bait pension fund investors. UETA includes promissory notes and documents of title in its definition of transferable records. E-SIGN strictly defines transferable records as promissory notes relating to a loan secured by real property.

“Overview of Revised UCC 9-105

-

The National Conference of Commissioners on Uniform State Laws (NCCUSL) revised UCC 9-105 to introduce the concept of an electronic chattel paper and to specify the legal requirements for having control over electronic chattel paper. The concept of having control over an electronic chattel paper is equivalent to the possession of a paper-based negotiable instrument under Article 3 of the UCC. However, since an electronic chattel paper is not “tangible” when compared to a paper chattel paper, UCC 9-105 imposes legal requirements to ensure that control can be asserted over a single “authoritative copy” of an electronic chattel paper. Since electronic records can be easily copied, UCC 9-105 established the legal foundation to ensure that the authoritative copy of an electronic chattel paper can be readily identified and that fraudulent copies cannot be easily transacted.

It appears the electronic registration makes it easier to securitize the notes and sell them to investors, but there is a requirement that the banks missed with their screw up of Mortgage Electronic Registration Systems, Inc. in the mortgages:

-

The legal requirements for electronic chattel paper as defined in UCC 9-105 are as follows:

“The Uniform Electronic Transactions Act (UETA)

The following definitions were extracted from the UETA text:

Transferable record means an electronic record that:

- (1) would be a note under [Article 3 of the Uniform Commercial Code] or a document under [Article 7 of the Uniform Commercial Code] if the electronic record were in writing; and

- (2) the issuer of the electronic record expressly has agreed is a transferable record.”

Overview of UETA Section 16

-

UETA Section 16 introduced the concept of a transferable record and leveraged the legal requirements for controlling an electronic chattel paper as defined UCC 9-105 to specify the legal requirements for having control over a transferable record. However, it restricted the scope of a transferable record to be an electronic record that is either a note under Article 3 of the UCC or a document of title (i.e. title) under Article 7 of the UCC. Hence, transferable records are electronic equivalents only to either paper promissory notes (i.e. negotiable instruments) or paper documents of title. UETA Section 16 also requires the issuer of the electronic record to explicitly agree that such a record is to be treated as a transferable record.

You can see that the “issuer” must “explicitly agree” that such a record is to be treated as a transferable record. At the turn of the century (13 years ago) the public was not ready for or willing to accept electronic signatures – especially on land transactions. And had Mortgage Electronic Registrations Systems, Inc. not run into road blocks due to its systemic corruption, greed and overall criminal activity it might succeeded in its ruse of creating three entities – all with the same name and four separate companies with the same acronym…all made to sound as if the borrower agreed to “electronic registration” – which nobody knew about or explicitly agreed to… and they would have gotten completely away with it until now!

You can see that the “issuer” must “explicitly agree” that such a record is to be treated as a transferable record. At the turn of the century (13 years ago) the public was not ready for or willing to accept electronic signatures – especially on land transactions. And had Mortgage Electronic Registrations Systems, Inc. not run into road blocks due to its systemic corruption, greed and overall criminal activity it might succeeded in its ruse of creating three entities – all with the same name and four separate companies with the same acronym…all made to sound as if the borrower agreed to “electronic registration” – which nobody knew about or explicitly agreed to… and they would have gotten completely away with it until now!

Now… we know about their patents which outlines their intent – and that appears to be to defraud homeowners and investors from the get-go.

UETA “SECTION 16. TRANSFERABLE RECORDS

(a) In this section, “transferable record” means an electronic record that:

- (1) would be a note under [Article 3 of the Uniform Commercial Code] or a document under [Article 7 of the Uniform Commercial Code] if the electronic record were in writing; and

- (2) the issuer of the electronic record expressly has agreed is a transferable record.”

To find your state’s UETA laws [click here]. Thank you, Professor.

Probably the most disturbing history lesson in researching the UCC was to learn that it was designed unbalanced to begin with where, of course, it benefits the commercial business side (banking) more than the consumer. Trying to find the definition of issuer, of course, was not an easy process. Definitions in state law are not clearly identified, if at all.

Probably the most disturbing history lesson in researching the UCC was to learn that it was designed unbalanced to begin with where, of course, it benefits the commercial business side (banking) more than the consumer. Trying to find the definition of issuer, of course, was not an easy process. Definitions in state law are not clearly identified, if at all.

“Issuer” means obligor, or the borrower aka “homeowner” as defined by E-Commerce: Financial Products and Services 2001, edited by Brian W. Smith, Appendix E, p. E-55-56. Page E-55:

“The purpose of the restriction is to assure that transferable records can only be created at the time of issuance by the obligor.” Ummmm… do you think maybe the MERS in the mortgages was conceived in fraud to slide in an explicit agreement signed by the borrower without his knowledge, or a definition or an explanation? How many homeowners looked at Mortgage Electronic Registration Systems, Inc. and wondered what a nominee was?! Page E-56:

It appears the MERS (III) mortgage loans were designed to be electronic records and electronically transferable which was necessary in order to sell, transfer and assign into securitized trusts. The homeowner agreed to the lender’s ability to “sell” the loan – but they never agreed to the securitization, electronic recordation, or electronic transfer-ability.

Maybe this is why all those original documents were being destroyed? As stated on page E-55: “the possibility that a paper note might be converted to an electronic record and then intentionally destroyed, and the effect of such an action, was not intended to be covered by Section 16.”

DOES THIS MAKE YOU RETHINK YOUR STRATEGY?

This information was never intended to be discovered by foreclosure defense attorneys or homeowners. Even government attorneys were not privy to patent information until it was called to their attention. “What do you mean the banks had patents? The USTPO is for inventions.”

Yeah, they had a huge invention – to RIG EVERYTHING, the contracts, the rates… The Biggest Financial Disembowelment Scandal Ever!

As Matt Taibbi so accurately put it: “The only reason this problem has not received the attention it deserves is because the scale of it is so enormous that ordinary people simply cannot see it.

As Matt Taibbi so accurately put it: “The only reason this problem has not received the attention it deserves is because the scale of it is so enormous that ordinary people simply cannot see it.

It’s not just stealing by reaching a hand into your pocket and taking out money, but stealing in which banks can hit a few keystrokes and magically make whatever’s in your pocket worth less. This is corruption at the molecular level of the economy, Space Age stealing – and it’s only just coming into view.” This quote is from the April 25th, 2013 issue of Rolling Stone.

____________________________________________________________________

Suggestions to consider for defense as a result of the UETA discovery

Consider adding a paragraph to your letter of dispute:

“Per your letter, my client demands proof of any and all assignments. Please send authenticated copies with the dates of the purported assignments. [Your State] has/has not adopted the Uniform Electronic Transaction Act [UETA] so use of electronic signatures in the assignment trail would be prohibited unless all parties to the transaction agree. [Your State UETA Code]. As you know, misrepresentation of ownership violates the Federal Fair Debt Collection Practices Act [15 USC 1692k et seq.] entitling the defendant to actual damages, civil penalties and attorneys fees.”

Be VERY Clear about the difference between MERS vs. MERS® in all of your correspondence and discovery:

Request for Admission No. 44: Admit that the plaintiffs’ original paper note was replaced with a digital version using electronic signatures.

Answer: ___ Admit ___ Deny

Request for Admission No. 45: Admit that the plaintiffs’ note was transferred via the MERS® eRegistry and eDelivery systems. See: http://www.mersinc.org/join-mers/mers-eregistry

Answer: ___ Admit ___ Deny

In any case, MERS just has too many dead ducks.

Thank you to everyone that reviewed and participated in this research and information. We all owe a debt of gratitude for those who have spent untold hours researching and investigating documents and theories so that others may have a better chance to win their own complaints and motions in court. Thank you for your kokua.

*Kokua is a Hawaiian word, that translates as “extending loving, sacrificial help to others for their benefit, not for personal gain…”

WOW! who’s on first, who’s on second and who’s on third? The best way to hide fraud and wrong doing is to cause confusion. Ya really think these sophisticated bankers and their lawyers did not have a purpose here? =)

And INTENT!

Virginia nailed this one and I thank you Virginia for your hours and yours going into years of dedication to expose this crime of terror by the banks on American soil. This is big! and I believe will turn the tides against MERS in all states as soon as it gets out.

More like Albert and Costello who’s on first. MERS will continue to be a nightmare in the mortgage industry because they function as simply a placeholder in the note for the banks and not a holder or beneficiary of the mortgages. MERS is nothing but a front company by the big banks who are shareholders of the company to profit and rip off the entire county recorder officers’ recording fees in this country.

MERSCORP was an undisclosed principal in the mortgage transaction. While the Lender and MERS knew that MERSCORP was going to hold the true document of title, in electronic format, the borrower never assented to such an agreement. In fact, the mortgage states that the applicable law would govern the document, not Virginia Law, which governs the MERS System and every transaction on it. Both MERS and the Lender entered into the agreement with unclean hands, with the knowledge and forethought of fraud in the factum.

When MERSCORP registered the mortgage, and made the electronic record, the transferable record, MERS did not surrender the tangible mortgage to them, or record any document that the tangible mortgage would cease to be the transferable record. MERSCORP, through fraudulent conversion by MERS and the Lender, created an electronic document of title, under UCC Article 7, to which it was the controlling party.

One GIANT PONZI CON ….. https://sites.google.com/site/thegreattexasbankjob/Home/speculation-bubbles-and-crashes-looting-101/fiat-money-notable-quotes

The Entire System is RIGGED ……. HELLO … http://www.youtube.com/watch?feature=player_embedded&v=uF9UJh8bU70

WATCH AND WAKE UP …. http://www.thedailyshow.com/watch/tue-december-7-2010/the-big-bank-theory

IN THE CIRCUIT COURT AND 20TH JUDICIAL DISTRICT

IN AND FOR LEE CO. FLORIDA

PATRICK LORNE FARRELL©, CONSOLIDATED CASES

Plaintiff, possessor, Droit-Droit 07-CA-14942 AND 07-CA-16767

vs. JUDGE FRANK PORTER

G.M.A.C.; WELLS FARGO, MARCH 30, 2012

IMPAC, et al, Defendants

PATRICK FARRELL’S ANSWER TO MORTGAGE FORECLOSURE COMPLAINT, AFFIRMATIVE DEFENSES; COUNTER-CLAIMS; RES JUDICATA;

REQUEST FOR JUDICIAL NOTICE OF IMPAC LETTERS

1. DENIED-IN REM is void as Farrell moved the note out of this Court’s Jurisdiction in JAN 2008.

2. DENIED- that the notice is lawful due to prior Fraud.

3. DENIED-Farrell executed a Security on OCT 11,2005. The allegations are unknown.

4. DENIED. Wells Fargo is not the holder, lender, mortgagee or creditor, their claims are a Fraud.

5. Admitted. #6- DENIED. #7.DENIED. #8. DENIED. #9 DENIED. #10.ILLEGAL. #11. DENIED. #12. DENIED. #13. DENIED. #14-UNKNOWN. WHEREFORE in paragraph #14- DENIED-Entire complaint based on a Fraudulent Security claimed to be a bank Note and Mortgage.

DEFENSES WHICH ARE CAUSES OF ACTION IN FARRELL V. GMAC, et al

__________________________________

Patrick Lorne Farrell in Propria Persona

Attorney In Fact/ Sovereign/Secured Party Creditor

signed “without the united states” and without prejudice/UCC 1-308

UCC-1 Filing # 2007-356-2344-8 [12/22/07]-Wash. St. -DOL

2904 NW14th Terrace-Cape Coral, Fl. 33993

Continue reading here.

Dr. Phillips,

The Ancient Roots of this Slavery are Being HACKED AT ……. http://www.bing.com/search?q=Ray+Fadden+++Six+Nations++Onchiota++Rainbow++&go=&qs=n&form=QBLH&pq=ray+fadden+six+nations+onchiota+rainbow+&sc=0-11&sp=-1&sk= SEE For Instance …. Founding Fathers, Secret Societies

http://www.scribd.com/doc/47571219/Founding-Fathers-Secret-Societies

Founding Fathers, Secret Societies – Read book online. SECRET SOCIETIES / HISTORY “The ultimate book about the secrets of our Founding Fathers. It is, very simply …

Yes I am Hawk Eye the Son of Swamp Fox ……

The Never Ending Story of Greed Corruption War Murder and The Corrupt Government Courts and Lawyers / Military that make it all possible

http://www.bing.com/search?q=American+Banking++Corruption+Fraud+Cover+Up++Judson+Witham&go=&qs=n&form=QBLH&pq=american+banking+corruption+fraud+cover+up+judson+witham&sc=0-19&sp=-1&sk=

Well said! ancient root of slavery! Otherwise those corrupted judges should be smuggled and exchanged with decent judges work for the victims not for the greedy banks & judges

ALL I CAN SAY IS “WOW”. VERY VERY GOOD JOB!

Thereis more info available with regards to this at http://www.ourlemon.com/ Trillion Dollar FUBAR- very in depth; needless to say all illegal. ALSO KEEP IN MIND as admitted in testimony most original notes were destroyed after scanning, which automatically cancells the note, it also means that all copies used as evidence in a case are counterfeit

While all of this information is interesting, it is not useful because it was never used in the mortgage industry. I am aware of only one transaction that became the first eNote and the collapse of the mortgage industry effectively put this idea way onto the back burner.

The fact is that this was their intention, but they got too greedy too quickly and their house of cards fell before they got to the eFraud level. I am sure they will try again soon though.

Click to access ProcessLoanNotPaperwork_Hultman.pdf

The first eNote was regestered in the eRegistry in 2007.

http://www.usfn.org/AM/Template.cfm?Section=Home&template=/CM/HTMLDisplay.cfm&ContentID=3888

This is where they were definately heading, lets try to make sure they don’t get there.

Pingback: ShellGame-MERS: Contrived Confusion – A MUST READ! | Deadly Clear

Pingback: Mortgage Crisis 101 by Prof. John Campbell | Deadly Clear

Pingback: Securitization is NOT a “Traditional Mortgage Loan” Operation | Deadly Clear

Pingback: “Height of Hypocrisy” – Legalize MERS with a National Mortgage Data Repository aka Foreclosure Fraud-Away | Deadly Clear

Pingback: MERS MONOPOLY & PATENTED SECURITIZATION? | TIERRA LIMPIA by Charles Lincoln

Pingback: Wall Street’s Mortgage Fraud Scandal. “You can have a house that is fully paid for and still end up in foreclosure” | Deadly Clear

Pingback: OCC – Correcting Foreclosure Practices | Deadly Clear

Pingback: TBTF HAS MET ITS WATERLOO | Deadly Clear

Pingback: THE HISTORY AND DEATH OF MORTGAGE ELECTRONIC REGISTRATION SYSTEMS, INC. ACCORDING TO THE USTPO | Deadly Clear

Pingback: Is the Promissory Note Even Enforceable? | Deadly Clear

Reblogged this on Deadly Clear and commented:

Since Yahoo seems to have a problem allowing the links to this post be emailed – it must be hitting a very hot button and time to Reblog the information.

Reblogged this on Justice League.

Incredibly fabulous and extremely useful fodder – D/C has combined some of its greatest articles – read this over and over cause there’s a lot to glean from it!

Thanks D/C for re-publishing this article – what a NUGGET as Dave Krieger from Clouded Title calls it!

Pingback: Policy Changes aka eNotes are Here! New Paragraph 11 in Promissory Notes. | Deadly Clear

Pingback: Saterbak Dissected – By Californians for Justice | Deadly Clear

Pingback: About Those PSA Signatures | Deadly Clear

USAA FEDERAL SAVINGS BANK v. ALEX BELFI, Case No.: 2:2019cv03607