Most New Century mortgages will find the same problem. Fraudulent assignments are not ministerial…

And which making it impossible for Carrington or Wells Fargo to legally enforce the lien.

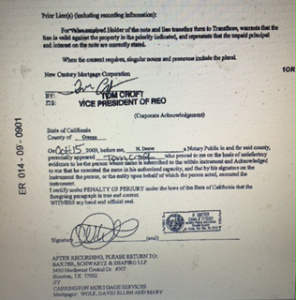

Wolf Transfer of Lien (NCMC to WF), 10.15.2009

Notice that from the Wolf vs. Wells Fargo lawsuit, the transfer of lien document was signed by Tom Croft, Vice President of REO for New Century Mortgage Corporation. Croft, according to Linkedin website of the Senior Vice President of REO for Carrington: https://www.linkedin.com/in/tom-croft-388a5613. There is a major problem: New Century filed bankruptcy in 2007 and Carrington Mortgage brought New Century. The second problem is the transfer of lien document was recorded in 2009. Here is the SEC filing for Carrington Mortgage Trust, Series 2006-NC3:

| 0001369384 | Carrington Mortgage Loan Trust, Series 2006-NC3 SIC: 6189 – ASSET-BACKED SECURITIES |